I. Introduction

The past couple of years have witnessed two major global crises in the COVID-19 pandemic (from March 11, 2020 when the World Health Organization declared COVID-19 a global public health emergency) and the Russia/Ukraine war (February 20, 2022-date). Although the two are non-economic phenomena (the former is a global health challenge and the latter is a geopolitical risk of global importance), both have significant impact on economies and markets. Given the similarities in the manner in which the COVID-19 pandemic and the Russia/Ukraine war have raised the risk levels in conventional financial markets such as equities, bonds, currencies, Exchange Trade Funds (ETFs), a study of this nature for precious metals (particularly, gold and silver) that have shown some resilience and proven as diversifiers and hedging assets is necessary (Adediran et al., 2021; Salisu & Adediran, 2020; Sikiru & Salisu, 2021; Shahzad et al., 2023). Further motivation for our study is that the crises induced by the COVID-19 pandemic and the war in Ukraine, through different mechanisms, raised inflation and inflation expectations in many countries including advanced and emerging economies, hence, it is worthwhile to recheck the inflation hedging powers of precious metals during these periods.

This study therefore contributes to the aforementioned studies by re-examining whether gold and silver still possess inflation-hedging potentials with comparisons between advanced and emerging economies and between the two crises episodes of the COVID-19 pandemic and the Russia-Ukraine war periods. The contribution is instructive for portfolio investment and policy direction in the countries examined. For instance, evidence of inflation-hedging would indicate the usefulness of precious metals as alternative options for financial investors in the countries under review. The study also informs relevant policy implications due to the dissimilar policy responses to the two aforementioned crises. For instance, the COVID-19 pandemic largely inspired quantitative easing and reduction in policy rates in many countries due to its recession-causing effects. On the other hand, many countries have been raising their policy rates to curtail the food, energy, and commodity hike effects of the Russia-Ukraine war.

In the results section, we document how gold (but not silver) retains its inflation-hedging powers during both the COVID-19 pandemic and the Russia-Ukraine war with implications for investments. The subsequent sections are as follows: Section II presents the methodology and data, Section III discusses the findings of this study, and Section IV concludes the paper.

II. Methodology and Data

We adopt a panel data framework to compare the inflation-hedging powers of gold and silver during the COVID-19 pandemic and the Russia-Ukraine war between G7 advanced economies [United States, United Kingdom, Canada, Japan, Italy, France, and Germany] and seven emerging economies [Brazil, India, China, South Africa, Turkey, Indonesia, and Nigeria]. The relevant data needed for the analyses are the country-specific year-on-year inflation data which are obtained from the Bank of International Settlement database [https://www.bis.org/statistics/cp.htm]. The global gold and silver prices used for the computation of the returns on precious metals come from the London Bullion Market Association AM fixings per troy ounce [https://www.quandl.com/data/LBMA/]. For robustness, we account for the role of the monetary policy environment in the economies by augmenting the model with the central bank policy rates of each country. This data also comes from the Bank of International Settlement [https://www.bis.org/statistics/cbpol.htm]. The data scope covers the period of the COVID-19 pandemic as well as the ongoing war in Ukraine, that is, from March 2020 to April 2023.

We adopt a panel threshold technique as informed by Salisu et al. (2020) which examines the inflation hedging potential of cocoa in net cocoa importing and exporting countries. In the present case, the panel threshold technique allows us to explore possible nonlinearities in the nexus between returns on precious metals and inflation in the economies under investigation. However, unlike Salisu et al. (2020), we employ the dynamic variant of the panel threshold model of Seo, et al. (2019) as follows:

\[\begin{aligned} {gold}_{it} &= \alpha_{gold} + \beta_{gold}{gold}_{i,t - 1} + \delta_{gold}\inf_{it}\\ & \quad + \theta_{gold}\left( \inf_{it} - \lambda_{gold} \right)1\left( \inf_{it} \geq \lambda_{gold} \right)\\ & \quad + \mu_{i}^{gold} + \zeta_{it}^{gold}\ ;\\ i &= 1,2,\ldots N;t = 1,2,\ldots T \end{aligned}\tag{1}\]

\[\begin{aligned} {silver}_{it} &= \alpha_{silver} + \beta_{silver}{silver}_{i,t - 1} + \delta_{silver}\inf_{it}\\ & \quad + \theta_{silver}\left( \inf_{it} - \lambda_{silver} \right)1\left( \inf_{it} \geq \lambda_{silver} \right)\\ & \quad + \mu_{i}^{silver} + \zeta_{it}^{silver}\ ;\\ i &= 1,2,\ldots N;t = 1,2,\ldots T \end{aligned}\tag{2}\]

Equations (1) and (2) specify the dynamic threshold regression models with a kink in inflation (the threshold variable) for evaluating possible nonlinearities in the nexus between returns on precious metals and inflation. and represent the returns on gold and silver prices, respectively, which are repeated across cross-section units to be consistent with panel structure of the country-specific inflation series which doubles as the threshold variable. is the value of the threshold variable when the analysis is divided into two regimes. The rest of the specifications signify the individual effects and the error term & respectively.

The computational details and the bootstrapping approach for estimating the coefficients and and for conducting the threshold effect test with the kink slope no threshold effect, and presence of threshold effect] are well documented in Seo et al. (2019). Readers may therefore refer to this for extensive details. To validate the inflation-hedging roles, the returns on precious metals have to be positively and significantly linked to inflation such that and indicate inflation hedging performance of gold and silver, respectively, and and suggest no hedging role (see Adediran et al., 2023).

III. Results

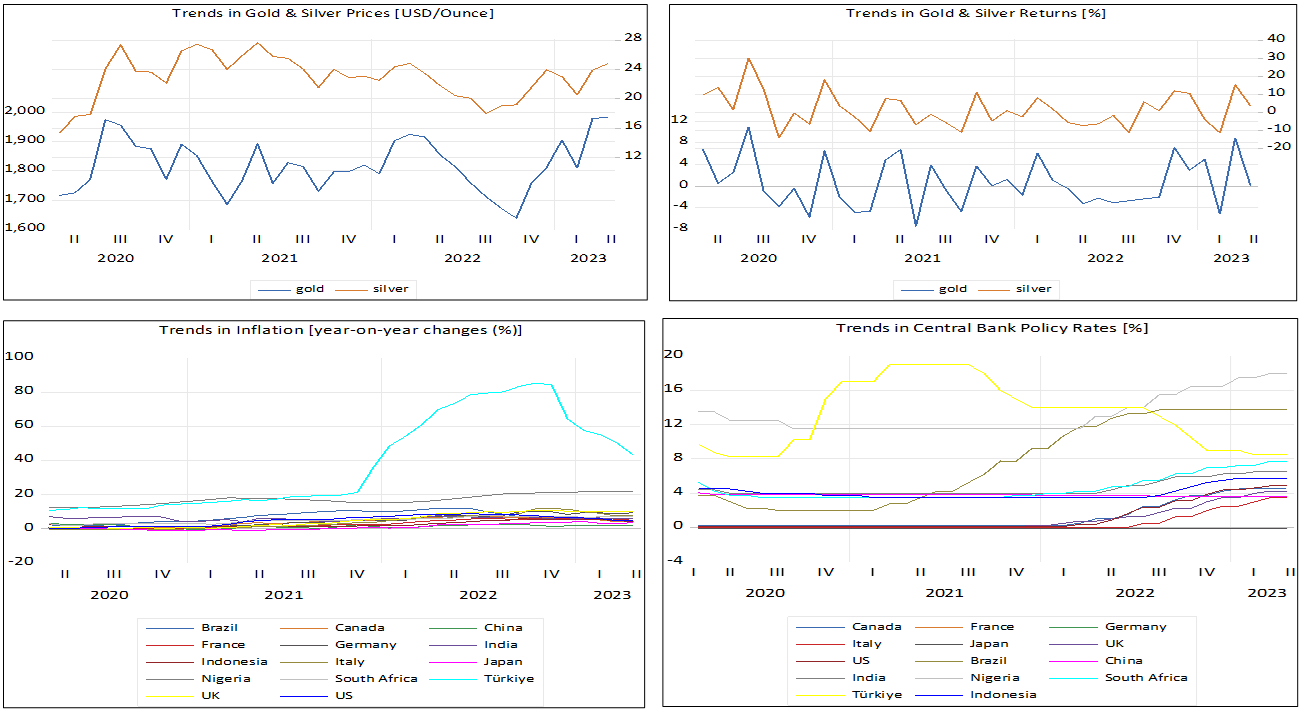

Some descriptive statistics are offered in Table 1 and Figure 1 from which we can draw salient information to inform the main analysis. As shown in the preliminary results, it is not strange that, on average, the price of gold far outpaces the price of silver on the international market. However, what is striking from the first quadrant of Figure 1 is that silver returns mostly exceed gold returns. From Table 1, we see clearly that silver performs better than gold in terms of returns during the COVID-19 pandemic while the two are close in terms of returns performances during the Russia-Ukraine war period. Based on the coefficient of variation statistic reported in Table 1, it is evident that the pandemic leads to higher volatility in gold returns than in silver returns, while the reverse appears to be the case during the war. The second striking observation is that the war in Ukraine has engendered higher inflation and monetary policy rate responses than it has during the pandemic among both emerging and advanced economies. Further, it becomes evident from the average values rendered in Table 1 that emerging economies are high inflation and high interest rate environments while advanced economies are low inflation and low interest rate environments (Adediran et al., 2022; Salisu & Vo, 2021). The insights obtained from the related literature and implemented in this study is that incorporating the policy environment in the analysis could aid in a better understanding of the macroeconomic dynamics being studied. This assertion was validated in this study.

From the main results in Table 2, we confirm the threshold effects in all the 16 subpanels evaluated to justify the choice of the dynamic threshold regression. The statistical significance of the kink slope coefficients iindicates the rejection of the null hypothesis that a linear model is efficient for rendering the relationship between returns on precious metals and inflation. Hence, the nonlinear model is preferred for evaluating the study’s objective. Of major importance are the delta coefficients given their relevance for gauging the inflation-hedging performances of gold and silver between advanced and emerging countries and between COVID-19 pandemic and Russia-Ukraine war subsamples. While the main results consider inflation series as the sole predictor and the threshold variable, for robustness, we account for the central bank policy rates in the estimations.

Results rendered in Table 2 inform us that gold retains its inflation hedging powers in hundred percent of the cases considered over the COVID-19 pandemic and Russia-Ukraine war periods. On the other hand, returns on silver fail to display inflation-hedging potentials in five of the sixteen cases considered (see Adediran et al. (2021) for evidence that although gold and silver perform as safe havens during the early days of the COVID-19 pandemic, gold outperforms silver in this regard). However, if we account for the interest rate environment as argued, we find out that silver loses its protection against inflation. Without this consideration, one might conclude that investors in emerging markets (as against advanced markets) could benefit from a portfolio that contains silver during the pandemic and the war. Hence, the role of the monetary policy environment of the economies appears to be relevant in similar empirical analysis. In other words, if we base the analysis solely on the models that include the central bank policy rates, we would conclude that unlike gold, silver has lost its protective powers during the COVID-19 pandemic and the Russia-Ukraine war, regardless of whether the investors are in emerging or advanced economies.

IV. Conclusion

Before now, precious metals, particularly gold and silver, appeared to have attained the status of safe havens useful for protecting investors against specific or systemic market risks. However, given the distortions in the global financial markets occasioned by the COVID-19 pandemic and Russia-Ukraine war, this study re-examines the inflation-hedging properties of precious metals in the face of the financial and macroeconomic glitches caused by the COVID-19 pandemic and the Russia-Ukraine war. Further, since the twin crises affect the inflation dynamics of countries with relevant monetary policy responses, the study re-assesses the hedging roles between advanced and emerging markets as low and high interest rate environments respectively.

The study adopts the dynamic panel threshold regression for estimation and confirms evidence of threshold effect in the data. The analyses are extensive covering comparisons between gold and silver, emerging and advanced markets, COVID-19 and the Russia-Ukraine war sample periods, and the inclusion or non-inclusion of the monetary policy environment. The overarching idea from the study is that only gold has retained its inflation-hedging powers whereas silver has lost these capabilities during the economic crises that accompany the pandemic and the war. The empirical contributions of this study have implications for further research. One of these is that similar analysis should reflect the policy environment of the market being studied.