I. Introduction

In the past couple of decades, the implications of global oil price variations on important macroeconomic indicators such as production, investment, consumption, inflation, and stock returns have gained considerable attention. Despite the growing literature on oil shocks across countries, limited attention has been paid to the link between oil prices and the external balances of economies. A spike in crude oil prices is regarded as a negative terms-of-trade shock in net oil-importing nations. To counteract negative terms-of-trade shocks, nations must borrow from foreign sources. According to Kilian et al. (2009), international risk sharing is inadequate, meaning that the ensuing imbalances may be insufficient to buffer the domestic effects of oil price shocks. Therefore, a better understanding of the impact of oil price shocks on trade balances in oil-importing countries is critical from both a policy and theoretical standpoint. Thus, the present study investigates the dynamic effects of global oil market shocks on India’s merchandise trade balance. India is the third largest consumer of crude oil and petroleum products after the United States and China. Crude oil products account for 26% of India’s total energy consumption. The majority of India’s crude oil demands are met by imports, making it one of the world’s largest crude oil importers (Pal & Mitra, 2016). Consequently, a greater share of crude oil in the import basket contributes to the current account deficits. India’ vast amount of crude oil imports directly links her trade balances to global oil market shocks, which exposes the Indian economy to oil market shocks. Therefore, a comprehensive understanding of the relationship between oil shocks and current account balances is essential for adopting appropriate policy measures to mitigate the negative consequences of oil shocks. This study contributes to the existing literature by analyzing the relative importance of oil-market shocks to explain various components of merchandise trade balances in India, using the impulse response and forecast error variance decomposition (FEVD) analyses.

Theoretically, changes in oil prices affect external balances via the trade and valuation channels. Since crude oil is critical in the manufacturing process, an oil price increase can result in an increase in input costs and a decrease in real GDP, forcing the country to reduce exports (Le & Chang, 2013). Thus, an exogenous increase in oil prices is expected to have a negative impact on net oil importers’ overall trade balance. Rising oil prices increase the import bills for crude oil, which can generate an immediate rise in the current-account deficit (trade channel). The influence of oil price shocks through the valuation channel depends on how sensitive asset prices are to oil demand and supply shocks. An oil shock might generate a short-term financial loss by altering the asset-holding positions of oil-exporting and oil-importing nations (Kilian et al., 2009). In the real world, where financial markets are imperfect, the wealth disparity between oil-importing and oil-exporting nation blocks determines the effects of a permanent spike in oil prices on trade balances (Bodenstein et al., 2011). According to Bodenstein et al. (2011), an adverse oil price shock can worsen trade imbalances in oil-importing nations in an imperfect market.

Few empirical studies have attempted to unravel the nexus between oil shocks and trade balances. For instance, Kilian et al. (2009) and Le & Chang (2013), using the Structural Vector Autoregression (SVAR) model, found that oil-market shocks significantly influence the external balances of oil-importing and oil-exporting countries. Rafiq et al. (2016), Jibril et al. (2020), Baek & Kwon (2019), Baek et al. (2019), and Ahad & Anwer (2020) reported asymmetries in the impact of oil price changes on the trade balances of various countries. Arouri et al. (2014) and Nasir et al. (2018) found, via the VAR model, that a rise in oil prices deteriorates the trade balance in India. Similarly, Sahoo et al. (2020) found a negative effect of oil prices on the current account balance, using the autoregressive distributed lag (ARDL) model. The existing studies in India have not investigated the effect of various forms of oil-market shocks on the trade balance. Oil-market shocks, such as oil supply, aggregate demand, and oil-specific demand shocks have differing (or various individual) effects on trade balances and other important macroeconomic variables (Kilian & Park, 2009). Furthermore, the responses of the oil and non-oil components of the aggregate trade balance to oil market shocks may differ; this must be investigated further. The current research addresses this gap by analyzing the influence of oil market shocks, namely oil supply shocks, aggregate demand shocks, and oil-specific demand shocks, on the aggregate merchandise trade balance and its sub-components, namely oil and non-oil trade balances. The rest of the paper is organized as follows: Section II describes the data and methodology, Section III discusses the results, and Section IV concludes the study.

II. Data and Methodology

Monthly data on trade balances (aggregate, oil, and non-oil), nominal crude oil price (oil), global crude oil output (opd), and global real activity index (gra) are utilized from January 2001 to March 2020. The sample period was selected based on data availability. Besides data on nominal oil prices, all other data, such as export values (in million US dollars), import values (in million US dollars), and the nominal exchange rate between India and the US, were obtained from the Reserve Bank of India (RBI) and its publications. The data on the Brent nominal crude oil price (US dollar per barrel) and world crude oil output comes from the U.S. Energy Information Administration (EIA) database. We utilized the global real activity index as a proxy to measure aggregate demand for crude oil, which we obtained from the author Lutz Kilian’s website.[1] Trade balances (TB) are measured as the natural logarithm of the export-import ratio. We obtained real oil prices (roil) by multiplying nominal crude oil prices by the domestic exchange rate between India and the United States and deflating it by the domestic consumer price index (CPI).

We adopted a SVAR model similar to Kilian & Park (2009) and Kilian et al.'s (2009) studies to identify oil-market shock. The model is as follows:

A0Yt=α+N∑i=1AiYt−i+εt

where, is vector of endogenous variables, i.e., and ‘N’ is the lag length of the model. The variables and are the global oil production (oil supply shocks), the global real economic activity index (aggregate demand shocks), and the real crude oil price (oil-specific demand shocks), respectively, while is the measure of trade balance (aggregate, oil, and non-oil). The variable “” represents serially uncorrelated structural innovations. The relation between the reduced form and structural innovations in the model can be written as:

et=A−10εt

Following Kilian et al.'s (2009) study, three key points were considered while identifying oil market shocks: (1) Oil producers respond to both lagged aggregate demand shocks and oil-specific demand shocks; (2) oil-specific demand shocks will not reduce global real economic activity in the same period; and (3) the unexplained portion of oil price innovation due to oil supply shocks or aggregate demand shocks must be specific to oil-specific demand shocks. These restrictions imply the following recursive restrictions on the elements of matric in Equation (2):

et=(eΔopd1tegra2teroil3teTB4t)=[a11000a21a2200a31a32a330a41a42a43a44](εoil supply shock1tεaggregate demand shock2tεoil−specific demand shock3tεtrade shock4t)

The measures of trade balance such as the aggregate trade balance, oil trade balance and non-oil trade balance eventually get affected by oil market shocks contemporaneously. Given the main objective of our study, and following Kilian et al.'s (2009) study, we assumed other things such as economic activities, price level, exchange rate, interest rate etc., remain constant and included trade balance as the only measure in the oil market model to investigate its dynamic response to oil market shocks.[2]

III. Empirical Results

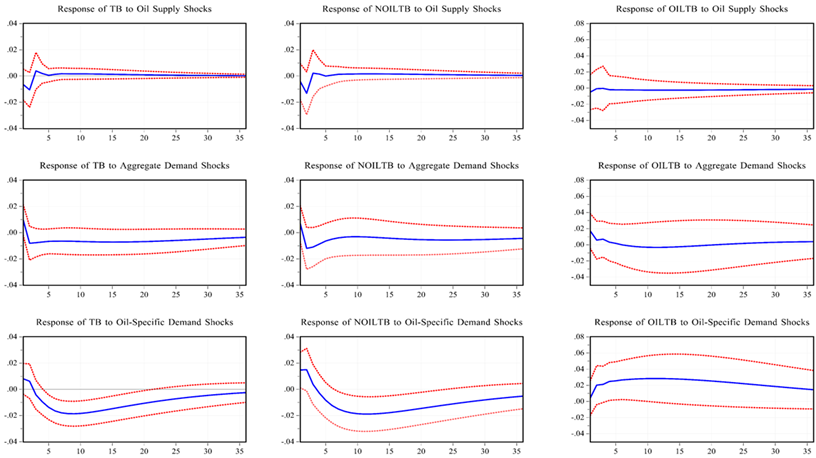

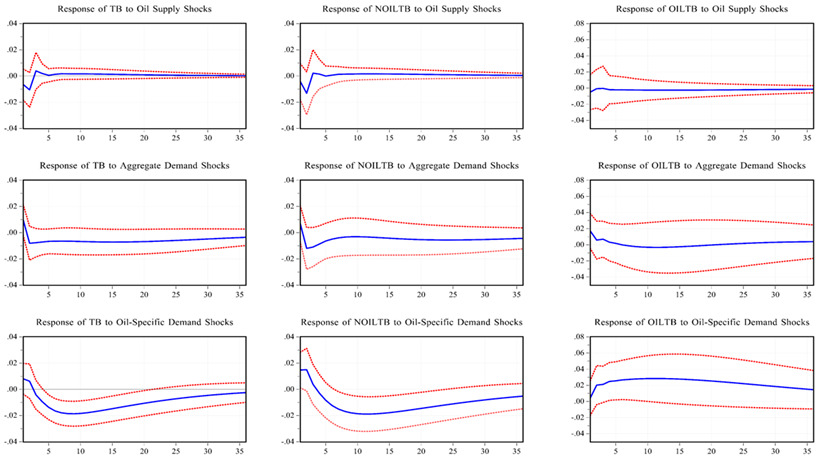

Since the VAR model requires stationary variables, we performed a battery of unit root tests. All the variables were stationary in the form expressed in equation (3).[3] Then, we estimated three distinct SVAR models to assess the response of three trade balance metrics (aggregate, non-oil, and oil) to oil shocks. An optimal lag length of 2 was selected for each model based on the Akaike Information Criterion (AIC). Figure 1 depicts the responsiveness of trade balances to oil market shocks. The responses of the aggregate trade balance to both oil supply shocks and aggregate demand shocks are observed to be insignificant in most of the forecast horizons. The impact of oil-specific demand shocks, on the other hand, is negative and significant across all forecast horizons. Such negative responses might be attributed to India’s excessive dependence on imported crude oil. The results are consistent with prior studies conducted in India (e.g., Arouri et al., 2014 and Nasir et al., 2018), which revealed that adverse oil shocks have a significant impact on India’s trade balance.

The responses of non-oil trade and oil trade balances to oil-specific demand shocks are statistically significant. Non-oil trade balances respond negatively to oil-specific demand shocks, whereas oil trade balances respond positively. In other words, rising oil prices worsen the non-oil trade balance while improving the oil trade balance. This result is not surprising, as India refines and sells a part of its oil imports to foreign nations. Thus, a positive shock in oil prices would impact revenue, increasing the value of total oil exports compared to total oil imports and improving the oil trade balance. The reactions of the oil and non-oil trade balances to both aggregate demand and oil supply shocks seem to be insignificant as the confidence bands are wider. The FEVD of trade balances suggests that oil-market shocks account for more than 30% of their overall volatility in the 36th period, with oil-specific demand shocks accounting for more than half of that (Table 1). Oil supply shocks and aggregate demand shocks play a minor role in explaining the variation of trade balances.

IV. Conclusion

This study used structural VAR models to investigate whether India’s merchandise trade balances respond differently to oil market shocks. The results from the impulse response analysis suggest that among oil market shocks, oil-specific demand shocks adversely influence India’s aggregate and non-oil trade balances. The effects of other oil market shocks on trade balances were statistically insignificant. The variance decomposition analysis further suggests that oil-specific demand shocks account for a major share of the total variation in all trade balance metrics. In summary, among oil-market shocks, only oil-specific demand shocks impact India’s economy. From a policy standpoint, we recommend that India minimizes its reliance on imported crude oil and uses alternative renewable energy sources to meet its domestic energy needs. This would help mitigate the unanticipated worsening of trade balances caused by adverse oil market shocks as well as other negative repercussions such as increasing inflationary pressures in the economy.

https://sites.google.com/site/lkilian2019/research/data-sets?authuser=0

Nonetheless, we also estimated the VAR models by including other variables such as output, inflation, and exchange and interest rates. The results are not reported as they were found to be almost similar to what we have reported in the present paper.

The results are not reported due to word limits and space constraints; they are however available upon request.