I. Introduction

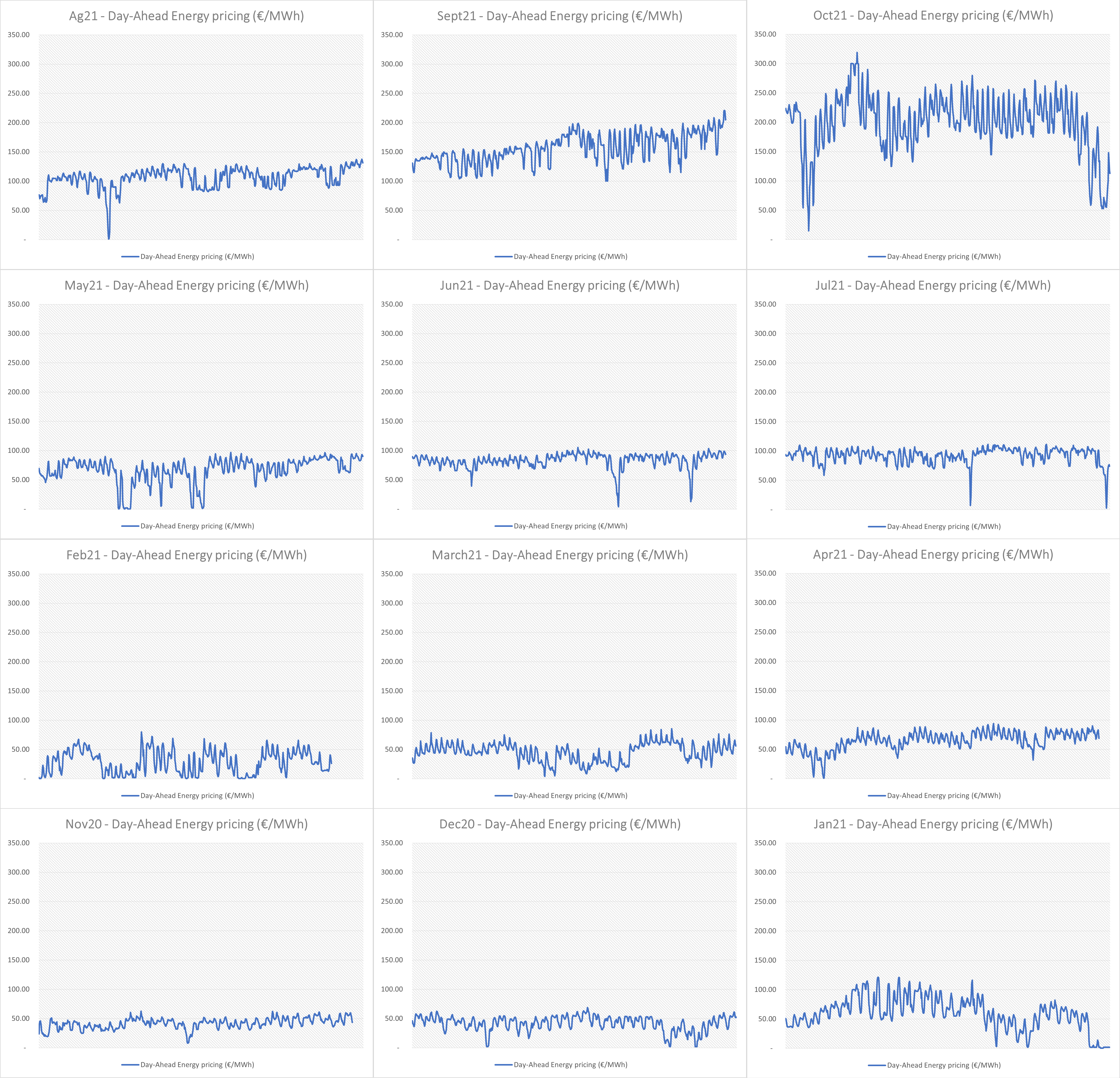

Energy is the cornerstone of modern economies, not only for the suppliers of physical goods and services, but also as a means of social welfare and comfort for people in general. Thus, an understanding of how price changes impact the energy demand of suppliers and consumers is very important (Gil-Alana et al., 2020). In the last year, energy prices in countries such as Spain and Portugal rose from approximately €50/ MWh in November 2020 to approximately €200/MWh by the end of October 2021, causing inflation tensions along the different elements of the supply chain. In European countries, the energy pricing strategy is fixed with day-ahead market systems (single-day-ahead coupling).

In the Spanish market, aligned with the objectives of the European Internal Energy Market (Directive 2009/72/EC), the Operador del Mercado Ibérico de Energía (OMIE) is the nominated electricity market operator for managing the day-ahead and intraday electricity markets by submitting selling and takeover bids with market-based supply prices. This market has a large number of regulatory specificities and competition constraints compared to other European energy markets. The main issues to be resolved in the Spanish market are the reduced competition with few suppliers, the tariff deficit due to past regulated prices below production cost, potential market integration between different players, and the introduction of new technologies to reduce CO2 emissions (Duarte et al., 2017).

Additionally, from a global perspective, a final challenge involves the interconnection networks with foreign countries as a protective measure. Currently, the European Union (EU) energy policies called for a well-integrated internal energy market in 2020 by achieving the interconnection of at least 10% of the installed electricity production capacity for all EU member states, with a 15% target in 2030 (Rubino & Cuomo, 2015). However, in the specific case of the Spanish market, these interconnections can be done only across the Pyrenees mountains, and thus there is a real risk of Spain become an energy island. An adequate cross-border interconnection capacity should help to avoid the internal development of dispatchable reserve capacity, for balance and grid security purposes. N. C. Figueiredo et al. (2015) tracked the Spanish case, showing that Spain has already surpassed this value, reaching 25.6%, and is aiming to achieve 3,000 MW in the near future, which will represent 32% of the maximum demand considered in this study; however, by 2020, overall consumption was still locally fulfilled.

Several authors have recently investigated the Spanish market and its peculiarities. In terms of the green renewal process R. Figueiredo et al. (2019) studied the replacement of traditional coal-based power plants with photovoltaics, while Pereira and Saraiva (2013) explained the implications of the penetration of wind power. Ciarreta and Zarraga (2010) studied the dynamic relation between electric consumption and the gross domestic product, and, more recently, Ciarreta and Zarraga (2016) examined the volatility of the intra-day electricity market. Rubino and Como (2015) explained interconnection needs, Capitán Herraiz and Rodriguez Monroy (2013) studied the futures market, Gil-Alana et al. (2020) examined the relation between energy consumption and prices in both the futures and spot markets, and Lagarto et al. (2014) studied the market power of generating firms in the day-ahead market.

The objective of this paper is to evaluate the impact of shocks in the Spanish energy market by studying the degree of persistence in hourly energy prices during the last 12 months, to understand if shocks that are affecting this market are expected to remain permanent. From a methodological perspective, fractional integration will be used as a time series technique, allowing for a more flexible dynamic specification of the data time series than other approaches based on integer degrees of differentiation.

II. Data description and methodology

The data of this paper are based on 12 independent time series associated with the hourly pricing for each of the last 12 months (November 2020 to October 2021), with hourly records (00:00 to 23:00) of the spot day-ahead market price traded by OMIE. These series include both the shock of Storm Filomena last winter and the recent natural gas rally shocks. These 12 series of data provided by OMIE are plotted in Figure 1 and their descriptive statistics summarized in Table 1.

As far as the methodology is concerned, we use fractional integration, which is widely used in the analysis of energy prices. The applied model is the following:

y(t)=α+βt+x(t),(1−B)dx(t)=u(t),t=1,2,...

where refers to the observed data; and are unknown parameters referring to an intercept and a linear time trend; is the backshift operator, that is, and is integrated of unknown order that is estimated from the data; and is an uncorrelated zero-mean process.

This model is applied separately for each monthly datasheet, yielding 12 independent results. Here, the estimation of the differencing parameter is crucial. Thus, if in (1), and is said to indicate short memory, as opposed to the case of long memory that takes place when From a statistical viewpoint, the cutoff point is 0.5. Thus, if is covariance stationary; however, it becomes nonstationary for and even more nonstationary as we increase the value of where we note that the variance of the partial sum increases in magnitude with Finally, from a policy perspective, mean reversion occurs if and shocks will have permanent effects if

III. Empirical results

The results of this analysis appear to be quite similar over the 12 monthly series, with values ranging from 1.30 to 1.53, providing empirical evidence that all the series under study are highly persistent. Table 2 displays the estimates of in equation (1) under the assumption of white noise errors, capturing all time dependence with the differencing parameter Thus, there is clear evidence of non-mean reversion, since is greater than one in all cases, as well as in all confidence intervals. Thus, shocks affecting these series are expected to have permanent effects.

However, these results are in contradiction with the findings of Gil-Alana et al. (2020), who analyzed future pricing markets and found d values around 0.62 with confidence intervals between 0.58 and 0.68. Given that our study is conducted with daily observations, but at longer periods of analysis with higher frequencies, further research should clarify if this d is modified by using longer periods of analysis (longer periods of data) or by increasing the sampling rates (hourly or daily).

IV. Conclusions

This paper has examined the hourly structure of 12 months of energy price data in Spain by using a long memory model based on fractional integration. The results indicate that all series are very persistent, with values of the differencing parameter substantially and significantly higher than one, implying a lack of mean reversion and the permanency of shocks. These results, however, could be due to the high frequency of the data used in the application. Robustness tests were conducted allowing for autocorrelation in the error term, and the results were very similar to the main results of the paper, finding support for high levels of persistence. Nevertheless, further research should be conducted on this issue. Finally, because the data include the period of the COVID-19 pandemic, the high degree of persistence observed in the data indicates that the present shock could have a permanent effect on the series, implying the need for strong action to recover the original long-term projections.

Acknowledgment

Luis A. Gil-Alana and Miguel Martín-Valmayor gratefully acknowledge financial support from grant PID2020-113691RB-I00 funded by MCIN/AEI/10.13039/501100011033. Comments from the editor and an anonymous reviewer are gratefully acknowledged.