I. Introduction

In this paper, we examine how the US-China trade war, which began in 2018, has affected China’s energy transition and its ambition to become a leader in clean energy. The hypothesis posits that the trade war has served as a significant catalyst, boosting China’s leadership in renewable energy technologies and their deployment, rather than hindering it. This relationship between trade conflict and China’s progress in clean energy is grounded in Offensive Realism (Mearsheimer, 2001) and Mercantilist perspectives. These theories suggest that great powers tend to respond to external constraints and threats to their relative power with aggressive self-help measures, such as technological independence and dominance in key sectors, often engaging in trade wars. Testing this hypothesis is crucial because clean energy is now a key arena in great-power rivalry. It is essential to understand whether trade restrictions slow progress or unexpectedly accelerate it, as this has significant consequences for global decarbonisation efforts. It also affects supply chain security and shapes the strategic rivalry between the US and China.

We employ a mixed-methods approach, utilising secondary data from Chinese and US policy documents, trade statistics, investment flows, and production/export figures, spanning the period from 2018 to early 2025. The period from 2018 to the present is critically important for this discussion because it marks the exact timeline of the US-China trade war’s inception and escalation, which directly correlates with a pivotal acceleration in China’s clean energy strategy. We find that US tariffs and export controls have inadvertently propelled China toward greater self-sufficiency and market dominance in solar, wind, batteries, electric vehicles, critical minerals, and green hydrogen. The results remain consistent across both qualitative policy analysis and quantitative trends in capacity addition, investment flows, and export diversification.

The study’s findings make three significant contributions to the literature. Firstly, it links trade conflict to clean energy growth, an underexplored area in the international political economy. Secondly, the trade war marks a new phase, with clean energy becoming a key aspect of great-power rivalry, which is vital for understanding the global shift towards decarbonisation. Thirdly, it highlights the risks associated with relying on China for critical clean energy components and suggests policies for cooperation amid rising protectionism.

The rest of the paper is organised as follows. Section II discusses data and methodology used in this study, following by a discussion on main findings in Section III. The final section concludes the paper.

II. Data and Methodology

A. Data

The data utilised in this study is secondary and has been sourced from publicly available government policies, trade data, and investment statistics to trace trends in China’s renewable energy production, exports, market diversification, and its impact on the global market. Key sources include the Institute for Energy Economics and Financial Analysis, Statista, the International Energy Agency, Shanghai Metals Market, the International Aluminium Institute, the United States Geological Survey, and the Office of the United States Trade Representative.

B. Methodology

This article examines the impact of the trade war on China’s clean energy sector using a mixed-methods approach. The qualitative analysis reviews Chinese and US policy documents and trade literature, focusing on strategies such as Dual Circulation, the 14th Five-Year Plan, and the Clean Energy Consumption Action Plan. The quantitative analysis considers trade data, including US tariffs on Chinese solar panels and batteries, the diversification of LNG and crude oil imports, and global investment in renewable energy. It also utilises trade and production data from industries such as electric vehicles and batteries, with straightforward mathematical calculations applied to analyse these data sets. This approach provides a comprehensive assessment of how trade conflict influences China’s investments, market diversification, and technological advancement.

III. Main Findings

To counter the trade war, China adopted various strategies to ensure a reliable supply of fossil fuels while significantly expanding its renewable energy capacity. Although China’s drive towards clean energy began with the enactment of the Renewable Energy Law in 2005, it has seen considerable growth in renewable resources in recent years (Schuman & Lin, 2012). In 2018, the Clean Energy Consumption Action Plan (2018–2020) was introduced to establish a long-term framework for promoting the adoption of clean energy.

The USA imposed a 100% tariff on Chinese EV imports, 50% on solar cells, and 25% on EV batteries, critical minerals, and other products. These measures indicate a protectionist approach, with states striving to maintain hegemony in particular industries. In response to US tariffs, China’s Politburo introduced the Dual Circulation strategy on 30/07/2020 to protect its market. This focused on domestic economic resilience and Beijing’s global role through increased trade, investment, and openness. The policy spurred energy demand, driving government investments in green technologies such as hydrogen, solar, energy storage, and electric vehicles.

China’s 14th Five-Year Plan (2021–2025) emphasises technological self-sufficiency, aiming to reduce reliance on global technology and trade risks. It proposes major investments in renewable energy, mobility, storage, and ultra-high voltage transmission to boost demand for batteries, raw materials, and copper, supporting China’s energy transition, security, and decarbonisation. The plan advocates diversifying oil and gas sources and securing strategic channels. For example, domestic EV sales reached 31.4 million units, highlighting China’s focus on boosting consumption.

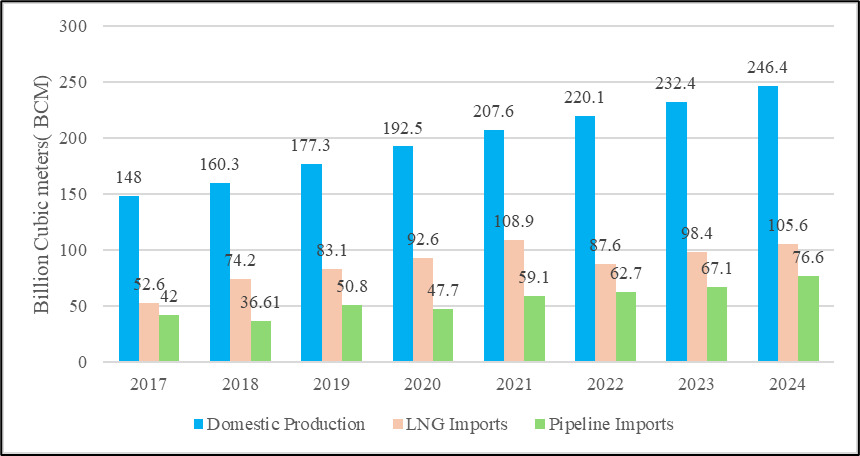

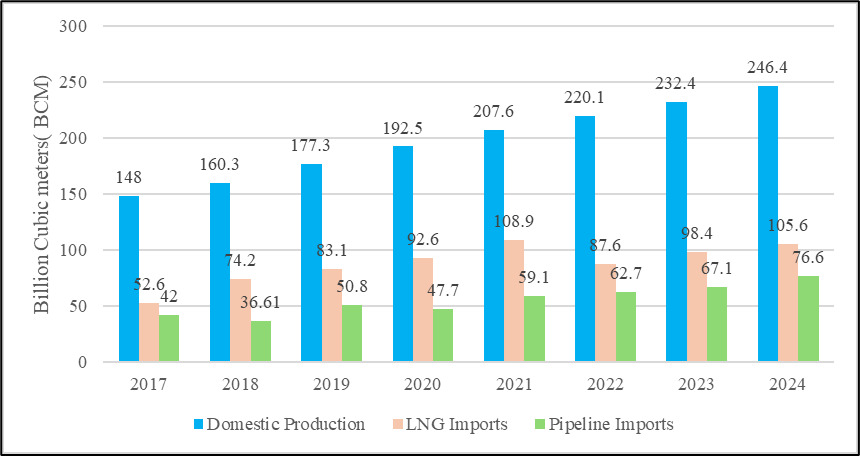

LNG is essential to China’s clean energy strategy. Before the trade war, the US was a major supplier of LNG. Following tariffs, China diversified its imports from Qatar (via a 27-year agreement), Russia, and Australia, alongside pipeline supplies from Turkmenistan, Kazakhstan, Uzbekistan, and Myanmar. In 2023, China restructured its natural gas market by increasing domestic production, adopting new technologies, and revising pipeline tariffs to expand supply and cut costs, meeting 60% of demand domestically. Figure 1 shows that Beijing’s energy production goals have improved, with LNG’s share rising from 22% in 2017 to about 25% in 2024. This reflects China’s aim to diversify its supply via global LNG markets. Amidst trade tensions, China reduced its US crude oil imports by 90% from 2023 to 2025, redirecting 1.2 million barrels per day to other suppliers. China also increased imports from Malaysia, Oman, and Iraq, while Canada benefited from the Trans Mountain expansion.

The U.S. imposed high tariffs on Southeast Asian solar cells, alleging that Chinese producers in Malaysia, Cambodia, Thailand, and Vietnam sell at a loss with unfair subsidies, thereby undermining U.S. competitiveness. Offensive Realism and Mercantilism view U.S. tariffs and China’s response as a power struggle in an anarchic world where states prioritise survival and relative power. China dominates the solar industry; in December 2024, Brazil, the Netherlands, India, Saudi Arabia, and Spain accounted for 42% of Chinese module imports. Through the BRI, China controls a significant share of Africa’s solar market, aiding its clean energy goals.

The U.S. imposed a 93.5% provisional duty on Chinese graphite imports. China retaliated with export licences for critical materials like tungsten, molybdenum, and rare metals used in chips, batteries, and green tech. China’s 40% share of global exports equates to about 1.25 million electric cars. By 2023, its EV battery production had surpassed 70%, and its large domestic EV market strengthened internal circulation, protecting it from trade shocks.

The ‘One Big Beautiful Bill Act’ in the U.S. eliminates tax credits for clean energy products, which could present further difficulties for clean energy producers and consumers. Importantly, it is expected to give China a stronger advantage over the U.S. in the global race to lead the growing clean energy technology market. Additionally, the trade war has disrupted the development of the real economy in the U.S. more than in China (Wang et al., 2025).

Although China remains the world’s largest greenhouse gas emitter, its rapid decarbonisation is remarkable. Policies under the 14th Five-Year Plan aim to increase annual domestic energy production to over 4.6 billion tonnes of standard coal by 2025. The plan emphasises expanding the proportion of non-fossil energy in total energy use to approximately 20%.

China has made significant advances in green hydrogen production. By April 2025, the industry had grown rapidly, adding over 82,300 metric tonnes of green hydrogen, 2.35 million metric tonnes of green ammonia, and 2.2 million metric tonnes of green methanol monthly. Projects in Inner Mongolia and Qinghai use alkaline electrolysers and PEM technologies, overcoming barriers to large-scale development and supporting transportation and industrial applications.

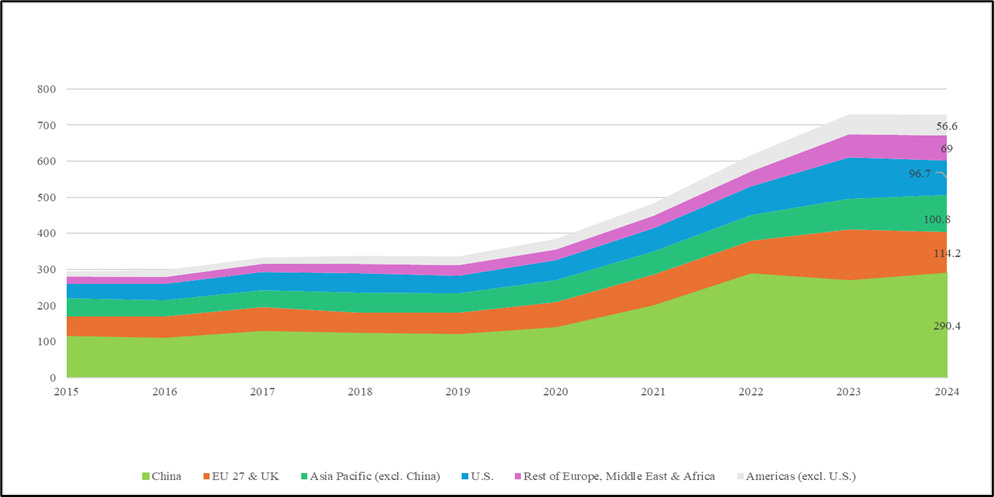

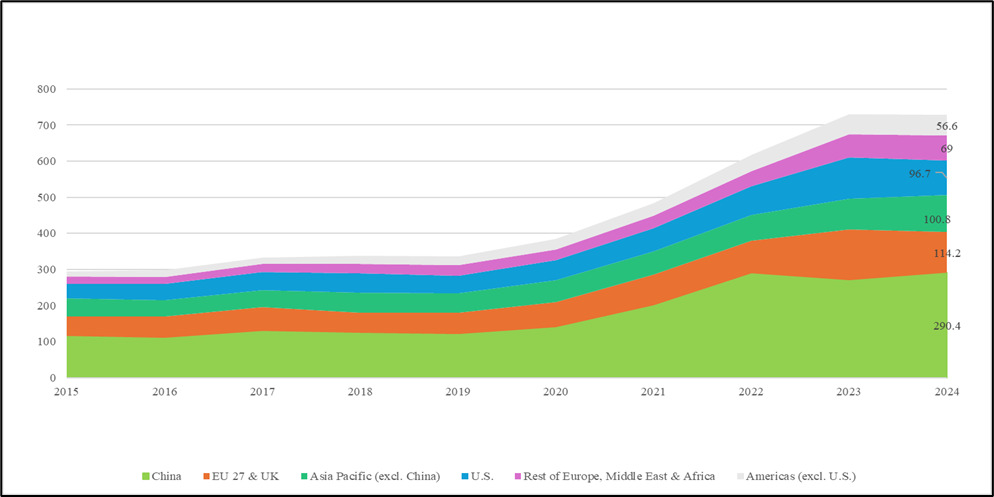

China invested $290.4 billion in 2024, surpassing all other regions by a significant margin. Its renewable investments are more than double those of the EU & UK, and nearly triple those of the U.S. This sheer scale of capital deployment sets a strong example and drives innovation. China is boosting its renewable energy leadership with 180 GW of solar and 159 GW of wind under construction. Wind and solar now account for 37% of power capacity, up 8% from 2022, and are expected to surpass coal (39%) next year. By 2025, China targets 200 GW of nuclear power and plans to replace its 2,990 coal plants with clean energy by 2060. With 57 reactors producing 55,762 MW and 30 more under construction for 31,953 MW, nuclear energy is key to its strategy.

China’s dominance in new energy technologies stems from controlling critical mineral supply chains, driven by decades of industrial policies, lax environmental regulations, and economies of scale. In 2024, it produced 21% of global bauxite, 60% of refined aluminium, and 98% of gallium, vital for solar panels, EVs, and fast chargers. It processes nearly half the world’s steel, zinc, and lead, over two-thirds of cobalt and lithium, 79% of battery-grade graphite, and 92% of rare earths for wind turbines and electric motors, strengthening its energy security and trade conflict position. However, its protectionist restrictions on critical minerals are seen as unjustified, hindering renewable energy deployment outside China and prompting diversification efforts such as the EU’s Critical Raw Materials Act.

In February 2025, China announced a plan to develop its new-energy storage supply chain to expand leading firms by 2027, boost innovation, competitiveness, and growth in high-end, innovative, green industries. It aims to secure lithium, cobalt, and nickel through local exploration, streamline mining rights, and encourage firms to diversify overseas projects to reduce costs.

China’s market diversification highlights the need for policies supporting long-term contracts and infrastructure, such as expanded pipelines under the BRI, to reduce trade and geopolitical risks. China is growing as a source of clean energy finance and technology transfer to developing countries through the BRI (Cheng & Wang, 2023). Some of China’s overseas energy investments, especially those under the Belt and Road Initiative, are structured as less concessional loans compared to development finance from other sources. This creates debt risk for recipient countries and gives China leverage over their long-term energy infrastructure development (Zou et al., 2022).

China’s LNG market diversification from the U.S. has bolstered energy security by reducing reliance on one supplier, supporting air quality goals by replacing coal with cleaner gas, and stabilising global energy markets by redirecting surplus LNG. China’s diversified markets ensure its energy needs are met and strengthen security against disruptions. The trade war, although unintended, spurred China’s renewable energy sector to become more resilient, geographically diverse, and technologically independent, accelerating its pace of energy transition.

China’s long-term planning, large-scale manufacturing, and strategic investments have built world-leading production capacity for solar panels, wind turbines, and lithium-ion batteries. This scale lowers global costs, making solar and wind power more affordable, especially in emerging markets, with Chinese manufacturing reducing solar panel prices.

China faces internal challenges, including uneven energy resource distribution. Relocating energy-intensive industries from coastal to renewable-rich central and western regions could ease grid bottlenecks caused by limited transmission and storage capacity. This would boost local economies, create jobs, and improve green energy use, reducing long-distance transmission pressure. Rapid renewable energy growth has some negative aspects as well. Rare earth mining has caused severe soil and water contamination, ruined farmland, and affected drinking water in areas like southern Jiangxi Province (Hao et al., 2015). Reports suggest the Clean Energy Consumption Action Plan impedes Sustainable Development Goals (Ai et al., 2025). Growing wind and solar energy are wasted due to inadequate grid capacity. China relies on coal for stability and peak demand. These issues push China to adopt policies boosting renewables, aiming to surpass coal by early 2025, and use the energy transition for economic resilience. They also require managing environmental impacts and international relations to prevent isolation.

China’s massive state-backed investments and subsidies have created extreme overcapacity in key sectors, such as solar panels, lithium batteries, and electric vehicles (EVs), flooding global markets with aggressively low-priced exports. Manufacturers in the U.S., Europe, and other countries find it nearly impossible to compete with the low production costs of Chinese firms, even with significant domestic incentives. A disruption in China due to political, natural, or trade issues could cripple the clean energy transition worldwide.

High tariffs on Chinese solar panels, batteries, and wind equipment raise costs, delaying clean energy adoption in the U.S.A. Europe faces slower impacts but remains vulnerable to prolonged escalation. In developing countries, especially African countries which rely on low-cost Chinese solar modules, higher project expenses threaten the affordability of solar energy. Overall, the global economic implications of the trade war are negative (Xia et al., 2019) and harm all economies, slowing down the clean energy transition (Li & Du, 2025).

IV. Conclusion

In conclusion, the trade war acted as a strategic catalyst for China’s energy transition. Although it caused some short-term disruptions, it ultimately reinforced China’s commitment to self-reliance and leadership in clean energy on the global stage. However, excessive reliance on China presents significant geopolitical and economic risks. Trade restrictions should be removed, and platforms such as the G20, ASEAN, and BRICS could promote cooperation by harmonising standards, aligning regulations, and establishing mechanisms for fair technology transfer. Strengthening technology sharing through frameworks like the Paris Agreement or the UNFCCC would assist countries in accessing green technologies and funding, fostering a more inclusive global clean energy ecosystem. Future research could explore how trade wars have accelerated China’s dominance in emerging and developing markets for its clean energy exports.

Acknowledgement

The authors would like to express their sincere gratitude to the reviewers and the editor for their insightful comments and constructive suggestions, which significantly improved the quality and clarity of this paper.