I. Introduction

Climate change stands as one of the most urgent challenges of the 21st century, with far-reaching consequences for the global economy (Olasehinde-Williams, 2024; Olasehinde-Williams & Saint Akadiri, 2025). The primary driver of this phenomenon is the increase in CO₂ emissions, largely due to growing energy demands and economies that still rely heavily on fossil fuels (Gozgor et al., 2018). CO₂ emissions play a major role in air pollution and the acceleration of global warming. Addressing this problem has become a worldwide priority in pursuit of sustainability.

A crucial solution lies in shifting from fossil fuels to renewable energy sources. By increasing the use of renewables, carbon emissions can be reduced, helping to mitigate climate change (Anwar et al., 2021; Gozgor, 2018). To address environmental concerns, international initiatives such as the Paris Agreement, the European Green Deal, COP27, and carbon taxes have supported sustainability efforts and promoted green finance. These efforts encourage investment in environmentally friendly markets and highlight the role of green finance in reducing pollution (Yousfi & Bouzgarrou, 2024).

However, changes in government policies—like adjustments in subsidies or environmental regulations—introduce uncertainty that can affect decisions made by consumers and investors (Bildirici et al., 2025; Olasehinde-Williams et al., 2023). Climate policy uncertainty (CPU) might actually have a positive impact on energy demand (Shang et al., 2022). Specifically, CPU can affect energy demand and clean energy investments through two main theoretical pathways. The first is policy-induced precautionary investment, where companies and investors—anticipating stricter regulations or carbon pricing in the future—redirect capital into renewable energy to hedge against regulatory risks. This approach demonstrates proactive, long-term planning in uncertain policy environments. The second is risk-driven pricing effects, where increased uncertainty raises the perceived risk of conventional energy assets, resulting in higher risk premiums and making clean energy options comparatively more attractive.

This study investigates the relationship between renewable energy consumption and prices, climate policy uncertainty (CPU), and CO₂ emissions in the U.S. by employing the quantile-on-quantile kernel-based regularized least squares method. This advanced approach allows for the exploration of complex and nonlinear relationships among the studied variables within the U.S. context. Unlike previous research, this study illustrates how uncertainty can stimulate clean energy adoption and influence green pricing strategies. It bridges a critical gap in the literature by connecting policy-induced uncertainty to environmental outcomes through the lens of energy markets. The research underscores the dual importance of policy and green finance as levers for advancing sustainability. Ultimately, it aims to inform more effective climate strategies that align economic behavior with environmental objectives.

Sections II, III, and IV provide information on data and methodology, empirical findings, and conclusions, respectively.

II. Data and Methodology

This analysis utilizes monthly U.S. data from November 2006 to August 2024, focusing on four primary variables: clean energy prices (CE), sourced from NASDAQ OMX (https://indexes.nasdaqomx.com/Index/History/CELS); renewable energy consumption (REC) and carbon dioxide emissions (CO₂), obtained from the U.S. Energy Information Administration (https://www.eia.gov); and climate policy uncertainty (CPU), derived from the Climate Policy Uncertainty Index (http://www.policyuncertainty.com/climate_uncertainty.html). CPU serves as a proxy for shifts in government policies pertinent to environmental regulation. The U.S. was chosen as the study context due to the availability of comprehensive CPU data. The sample period is determined by the earliest availability of clean energy price data.

While this study is centered on the U.S., its broader applicability to other countries should be considered cautiously. Climate policy uncertainty and energy market dynamics vary internationally, influenced by factors such as institutional stability, regulatory transparency, market structures, and the degree of policy integration. For example, emerging economies with weaker institutions or inconsistent policy environments might experience more pronounced adverse effects of policy uncertainty, whereas nations with strong policy credibility may see such effects diminished or delayed.

All variables undergo transformation into logarithmic first differences for analysis. Table 1 provides the summary statistics: CE, REC, and CPU have positive means, whereas CO₂ displays a negative mean. Results from the Jarque-Bera test show that all series depart from normality, with the exception of CPU.

This study uses a new econometric approach, the Quantile-on-Quantile kernel-based regularized least squares (QQ-KRLS), recently introduced by Adebayo et al. (2024). This innovative method combines the quantile-on-quantile (QQ) approach of Sim and Zhou (2015) with the kernel-based regularized least squares (KRLS) technique developed by Hainmueller and Hazlett (2014). KRLS, a machine learning method, is highly regarded for its flexibility in regression analysis, as it avoids rigid parametric assumptions. It employs Gaussian kernels to estimate the best-fitting function, thereby minimizing bias resulting from incorrect model specifications. Specifically, KRLS quantifies the influence of an independent variable X on a dependent variable Y as follows:

Es [^τyτxn]=−2σ2S∑n∑ijie||Xi−Xn||2σ2Xi−Xn

The average of the pointwise marginal effects of the independent variable on the dependent variable is expressed as where and represent individual observations and the sample size, respectively. Moreover, the QQ-KRLS technique allows for the evaluation of statistical significance across the entire distributions of both the independent and dependent variables[1]. This approach enables a nuanced exploration of complex or asymmetric relationships between variables, providing a comprehensive analysis of their interconnections. The final combined QQ-KRLS model is illustrated as follows:

Es [^τδyθτδxϑn]=−2σ2S∑n∑ijie||Xϑi−Xϑn||2σ2Xϑi−Xϑn

The average pointwise marginal effect of the conditional -th quantile of the independent variable on the conditional -th quantile of the dependent variable is expressed as Here, and represent the -th and -th conditional quantiles of the dependent and independent variables, respectively. However, it is important to emphasize that the QQ-KRLS method reveals patterns of dependence; therefore, the findings do not imply causality.

III. Empirical Findings

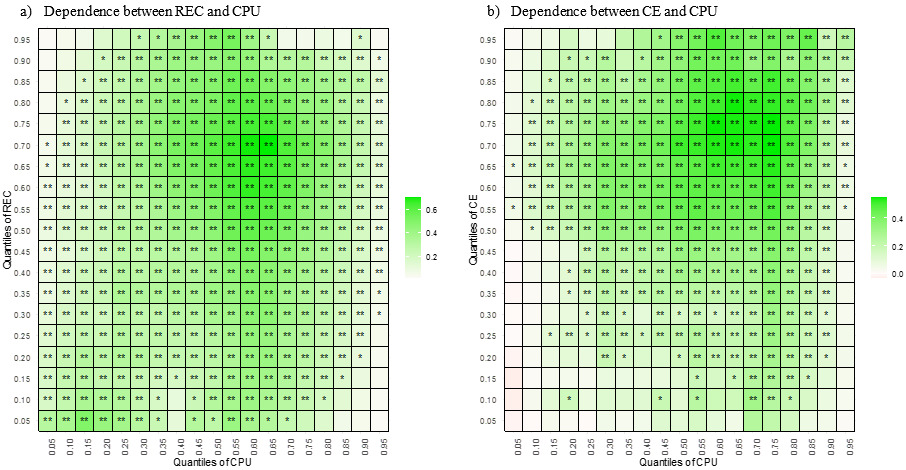

Figures 1 and 2 illustrate the dependence structure among the analyzed variables, displaying the mean pointwise marginal effect coefficients via color bars. These visualizations offer detailed insights into the nonlinear relationships identified in the study. Figure 1a depicts the quantile dependence between REC and CPU. The strength of this dependence ranges from 0 to over 0.6, as shown by the color scale. Results indicate a robust positive association across most quantiles of both variables, with particularly strong dependence—exceeding 0.6—at the upper quantiles (around the 60% and 70% levels) of both CPU and REC. This suggests that as climate policy uncertainty rises, renewable energy consumption also increases, likely reflecting anticipatory behavior by firms and investors in response to future regulatory risks. In most other quantiles, dependence lies between 0.2 and 0.6, indicating a positive but less intense association. However, weaker and largely insignificant dependence (below 0.2) is observed when REC is at its highest quantiles (85% to 95%) while CPU is low (5% to 15%), and vice versa. These nuances highlight asymmetric effects across distributions and suggest the relationship is strongest when both variables are elevated.

Similarly, Figure 1b shows the relationship between CE and CPU, with dependence values ranging from 0 to over 0.4. Like REC, CE exhibits a positive association with CPU across most quantiles, with particularly strong dependence (above 0.4) when both variables are at their upper quantiles (approximately 60% to 80%). Weaker and insignificant associations (below 0.2) occur when CE is low (5% to 45%) across various CPU quantiles, or when CPU is low (5% to 15%) and CE is high (80% to 95%). Moderate positive associations (0.2 to 0.4) are seen in the remaining quantiles. These findings support the idea that climate policy uncertainty boosts demand for clean energy assets, as such uncertainty increases the risks associated with fossil fuel investments and elevates the relative appeal of clean energy alternatives. The increase in CE prices during periods of heightened uncertainty may also reflect a shift in capital toward green finance markets by environmentally aware investors.

__clean_energy_prices_(c.png)

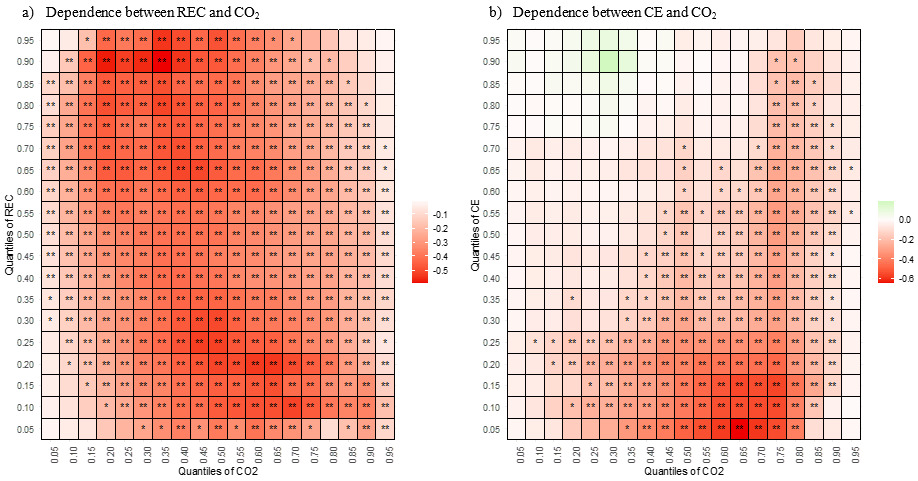

Conversely, Figure 2a investigates the dependence between REC and CO₂ emissions, where a significant negative association is found across a broad range of quantiles. The strength of this negative dependence ranges from 0 down to below -0.5, with the most pronounced inverse association (below -0.5) appearing at high REC quantiles (90% to 95%) and lower CO₂ quantiles (about 20% to 40%). This strong, negative relationship confirms that greater renewable energy consumption is linked to decreased carbon emissions. For other quantile combinations, the negative dependence remains, ranging from -0.1 to -0.5, revealing a persistent yet variable inverse association. Insignificant dependence is mainly observed at the extremes—when both REC and CO₂ are either very high or very low. Overall, the results affirm the environmental benefits of expanded renewable energy consumption, especially in effectively reducing CO₂ emissions at high consumption levels.

__clean_energy_prices_(c.png)

Figure 2b focuses on the link between CE and CO₂ emissions, revealing a significant negative association with dependence ranging from 0 to below -0.6. The strongest negative dependence (exceeding -0.6) occurs when CE is at its lowest quantile (5%) and CO₂ emissions are relatively high (around the 65th quantile). Another strong inverse relationship, ranging from -0.4 to -0.6, is found when CE is low (5% to 15%) and CO₂ is moderately high (50% to 70%). Across other quantiles, the negative dependence decreases gradually (from -0.2 to -0.4). Some combinations yield insignificant results, especially at the extremes of each variable. Nevertheless, the overall findings demonstrate that increases in clean energy prices are associated with reductions in CO₂ emissions, likely because rising green prices steer markets away from high-emission energy sources, capture the rising demand for sustainable options, and encourage a shift in investment behavior.

IV. Conclusion

This study examines the relationships among U.S. data on renewable energy consumption and prices, climate policy uncertainty, and CO₂ emissions. The findings reveal significant positive associations between climate policy uncertainty and both renewable energy consumption and clean energy prices, particularly at higher quantiles. This suggests that increased climate policy uncertainty drives up both renewable energy consumption and clean energy prices, underscoring the influence of policy uncertainty on the demand for renewable energy and green finance assets. In contrast, both renewable energy consumption and clean energy prices show a strong negative association with CO₂ emissions, highlighting their important role in reducing environmental pollution. These insights provide valuable guidance for policymakers and investors seeking to align climate policy, energy market dynamics, and sustainability goals.

The results further uncover a somewhat counterintuitive but clear positive relationship between rising climate policy uncertainty and increases in renewable energy consumption and clean energy prices. Two main factors explain these findings: precautionary investment and risk-driven pricing. Firms and investors may ramp up clean energy investments to hedge against future regulatory changes or to benefit from subsidies. However, such reactive strategies can sometimes lead to higher costs and strain supply chains. Additionally, elevated uncertainty can discourage long-term institutional investment, ultimately weakening systemic decarbonization efforts.

As such, climate policy uncertainty (CPU) should not be considered a deliberate policy tool, but rather a sign of an unstable policy environment. To effectively reduce CPU, policymakers should focus on creating stable, long-term regulatory frameworks, providing consistent tax credits and investment incentives, and offering proactive support measures—such as advancing complementary technologies and streamlining permitting processes. These steps are crucial for cultivating a predictable, low-risk investment climate that is essential for strategic, large-scale, and cost-effective decarbonization.

For more details about the QQ-KRLS method, please see Adebayo et al. (2024).