I. Introduction

The urgent transition to sustainable technologies hinges on the reliable supply of specific critical minerals indispensable for energy storage, electric vehicles, and renewable energy systems. However, these minerals—such as lithium, cobalt, nickel, rare earth elements, and graphite—are increasingly subject to the destabilizing effects of geopolitical risks. Recent conflicts, notably the Russia–Ukraine war, and evolving trade policies have underscored how geopolitical tensions can disrupt supply chains, elevate prices, and introduce significant uncertainties into the global market (Attílio, 2025; Nygaard, 2023; Olasehinde-Williams & Saint Akadiri, 2025; Pata et al., 2024).

In addition to direct geopolitical disruptions, protectionist commercial policies further complicate the landscape by restricting access to essential materials and inflating costs, undermining the broader objectives of sustainable technology development (Berahab, 2022). The rapid growth in global demand, driven by the expanding production of electric vehicles and renewable energy technologies, intensifies these market complexities, as shifts in political dynamics can lead to abrupt supply interruptions (Chishti et al., 2023).

Moreover, excessive reliance on mineral-rich but geopolitically volatile regions accentuates supply vulnerabilities. Recent studies emphasize diversifying supply sources and enhancing recycling efforts to mitigate these risks (Giuli, 2023; Nygaard, 2023). Quantitative analyses further reveal that geopolitical risks significantly complicate energy transitions, while also suggesting potential strategies for risk mitigation (Pozybill, 2022; Wang et al., 2024; Zhang et al., 2023).

This study employs KRLS and QR methods to address these challenges and capture geopolitical risk’s heterogeneous and nonlinear effects on energy transition minerals from 1961 to 2020. Our results indicate that while geopolitical risks significantly disrupt the market performance of cobalt, nickel, rare earths, and graphite, lithium and copper appear comparatively resilient, underscoring the need for targeted policy interventions.

II. Data and Methodology

A. Data

This study considers six key energy transition minerals: lithium, copper, cobalt, nickel, rare earths, and graphite. We measure geopolitical risk via the Geopolitical Risk Index (GPRI), a widely recognized measure of geopolitical risk in the academic and policy communities, originated by Caldara and Iacoviello (2022). The monthly data of the GPRI is obtained from [URL] and then converted into an annual frequency using the average observations method.

Table 1 reports the descriptive statistics of the gathered raw series from 1961 to 2020. Cobalt has the highest average, while the GPRI has the lowest. Rare earths have the highest coefficient of variation (CV), whereas GPRI has the lowest. The studied series, except for lithium, skew to the right. GPRI, copper, and graphite exhibit a platykurtic distribution, while other variables present a leptokurtic distribution. The estimates of the Jarque-Bera test reject the normal distribution for cobalt, nickel, and rare earths. In contrast, the ARCH-LM test strongly rejects homoscedasticity for all series. We take the logarithm of the series not only for non-normality and heteroskedasticity but also for elasticity.

B. Methodology

The KRLS model for this study is specified as follows:

Yit=f(Xt)+εt

where is the price or market dynamics of energy transition minerals, includes GPR. is a flexible, nonlinear function estimated using KRLS, and is the error term. The KRLS estimator solves:

ˆβ=argminβn∑i=1(Yit−K(Xt, Xj)β)2+λ‖

where is the kernel function (commonly a radial basis function or polynomial kernel), and is the regularization parameter to prevent overfitting. This approach captures geopolitical risk’s nonlinear and heterogeneous impact on energy transition minerals. Instead of mean-oriented traditional or machine learning models, KRLS allows us to examine the effects of GPR on each observation of the energy transition minerals based on automatic regularization that reduces overfitting.

III. Results

Figure 1 illustrates the pointwise marginal effects of GPR on each of the six energy transition minerals—lithium, copper, cobalt, nickel, rare earths, and graphite—using KRLS. Broadly speaking, each panel’s vertical axis indicates how a slight change in GPR is predicted to affect a specific mineral’s price (or returns) at each observation in the dataset. The red dots represent these observation-specific effects, while the blue smoothed line shows the overall trend. The figure underscores the heterogeneous and sometimes nonlinear ways that geopolitical tensions can influence different minerals, aligning with the broader literature on commodity risk responses (Caldara & Iacoviello, 2022).

A closer look at the panels reveals that certain minerals, such as lithium and graphite, exhibit a mild U-shaped relationship with GPR. At lower price levels, the marginal effect of GPR tends to be weakly negative or close to zero, but it becomes more positive as the market environment tightens.

This pattern suggests that when demand and prices are relatively subdued, geopolitical tensions do not dramatically affect prices—possibly because market participants do not foresee immediate supply constraints. However, as prices and demand increase (often coinciding with heightened concerns about supply bottlenecks), higher GPR can magnify fears of disruption, thus exerting a more substantial upward influence on prices. In contrast, metals like copper and nickel appear to experience wave-like or cyclical effects: moderate geopolitical risks may initially weigh on industrial demand and dampen prices. However, concerns about potential supply shortages can push prices upward if tensions intensify. Nevertheless, protracted or severe tensions might eventually curb economic growth and global trade, reverting the marginal effect to neutral or negative. These cyclical patterns are consistent with findings by Martino and Parson (2013), who highlight how both demand- and supply-driven factors can oscillate in response to escalating geopolitical risks.

Cobalt and rare earth, known for their concentrated supply chains (e.g., cobalt’s heavy reliance on the Democratic Republic of Congo and rare earth’s dominance by China), exhibit inverted U-shaped or near-flat patterns, respectively. The inverted U-shape for cobalt may stem from moderate geopolitical risks sparking concerns over supply disruptions—raising prices—while extremely high tensions might trigger a broader economic slowdown that reduces overall demand. Rare earth, by contrast, hovers close to zero or slightly harmful in marginal effects for much of the sample, reflecting a balance between supply-side vulnerabilities and demand-side uncertainties. Past studies (Mancheri et al., 2019) also show that rare earth markets are prone to policy-driven price shocks, which can amplify or dampen global risk effects depending on whether demand remains robust. Ultimately, Figure 1 emphasizes the importance of analyzing each mineral’s unique market structure and supply chain concentration when assessing the impact of geopolitical risk. By examining the data at each point rather than relying on mean-oriented methods, KRLS reveals these nuanced patterns, demonstrating that geopolitical tensions can trigger upward and downward pressures on energy transition minerals depending on prevailing market conditions.

Table 2 summarizes the average marginal effects of geopolitical risk on each energy transition mineral. Except for Lithium (−0.016, statistically insignificant), all minerals show a negative relationship with geopolitical risk. Specifically, copper (−0.308) is significant at the 10% level, while cobalt (−0.113), nickel (−0.312), rare earth (−1.176), and graphite (−0.360) are significant at the 1% level. These results indicate that, on average, increases in geopolitical risk tend to depress the prices (or returns) of most energy transition minerals. The powerful negative effect on rare earths may reflect their concentrated supply chains and susceptibility to policy disruptions, a finding consistent with Mancheri et al. (2019). Similarly, the adverse impacts on copper and nickel echo the observations of Martino and Parson (2013), who noted that heightened uncertainty can dampen industrial demand and disrupt commodity markets. Furthermore, the overall negative associations align with Caldara and Iacoviello’s (2022) broader findings on how geopolitical shocks affect asset prices. Thus, these average marginal effects underscore the pervasive influence of geopolitical risk on the performance of critical energy minerals, highlighting the complex interplay between political instability and commodity market dynamics.

A. Robustness check

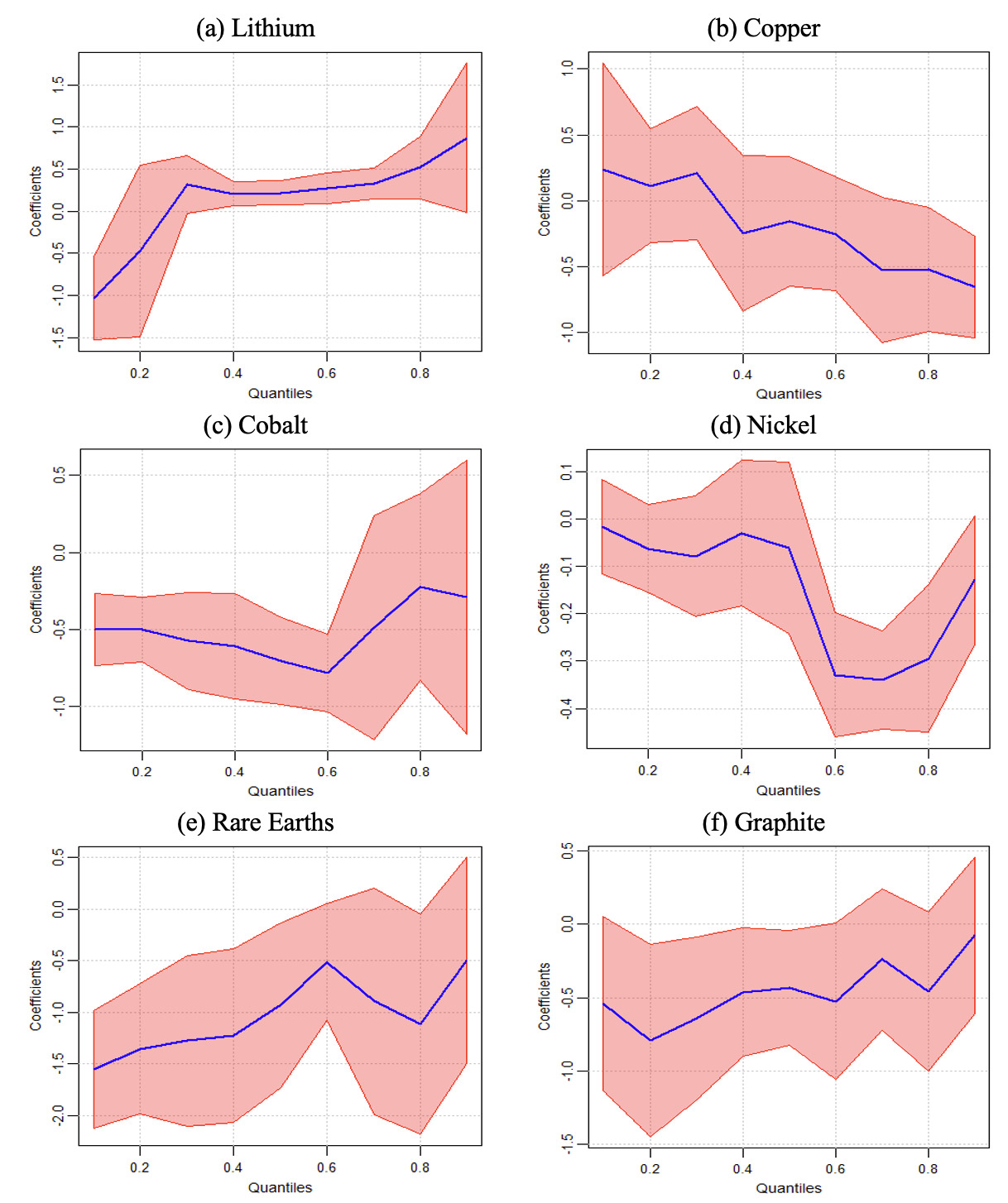

Figure 2 shows the QR coefficients for six minerals—lithium, copper, cobalt, nickel, rare earth, and graphite—as a robustness check for the KRLS findings. The horizontal axis denotes the quantiles of the dependent variable (e.g., returns), and the vertical axis indicates the effect of GPR. The shaded area represents 95% wild bootstrap confidence intervals.

The QR results reinforce that GPR has heterogeneous, often nonlinear effects across the conditional distribution of each mineral’s prices or returns. Lithium exhibits near-zero effects at lower quantiles but rises at higher quantiles, matching KRLS results showing greater sensitivity when prices are elevated. Copper and nickel present negative or neutral impacts in some quantiles and positive impacts in others, consistent with their cyclical industrial usage patterns: moderate geopolitical tension can dampen demand, while severe tension may tighten supply and lift prices.

Cobalt and rare earths exhibit similar variability, with cobalt’s effects shifting from near-zero to more pronounced at specific quantiles. In contrast, rare earths dip at mid-quantiles before recovering at the extremes. These patterns mirror their supply-chain concentration and policy-driven risks. Graphite reveals negative coefficients at lower quantiles, turning positive as quantiles rise, indicating that stronger demand amplifies the impact of GPR. Overall, Figure 2 corroborates the KRLS conclusion: geopolitical risk’s influence on energy transition minerals is not uniform. By highlighting distribution-specific effects, the QR approach underscores that policymakers and market participants must account for varying market conditions and supply-demand dynamics to manage geopolitical uncertainty effectively.

Table 2 provides the rolling window regression estimates for each of the six minerals—lithium, copper, cobalt, nickel, rare earth, and graphite—illustrating how GPR effects change over time. Each panel plots GPR coefficients derived from regressions estimated on moving windows (e.g., five- or ten-year periods), enabling us to observe shifts in sensitivity across different historical contexts. The magnitude and direction of these coefficients vary substantially. Lithium exhibits modest effects in earlier decades but shows sharper fluctuations in the 2000s and 2010s, likely to reflect its growing importance in battery and electric vehicle technologies. Copper and nickel, central to traditional industries, demonstrate cyclical patterns corresponding to broader economic cycles.

Meanwhile, cobalt and rare earth—often sourced from geopolitically sensitive regions—experience pronounced volatility, with coefficients turning sharply positive or negative during heightened global tensions. Graphite consistently shows adverse effects, although their negativity changes over time, indicating that GPR regularly dampens graphite market performance to varying extents. These rolling estimates highlight that geopolitical risk impacts are dynamic rather than static, influenced by evolving market structures, technological shifts, and macroeconomic conditions. Monitoring these temporal patterns is essential for anticipating supply-chain disruptions and developing adaptive strategies to manage critical mineral vulnerabilities.

IV. Conclusion

This study’s KRLS and QR findings confirm that geopolitical risk exerts heterogeneous and often nonlinear effects on energy transition minerals. While cobalt, nickel, rare earth, and graphite exhibit stronger negative responses, lithium and copper appear comparatively less sensitive. The QR estimates further reveal that the magnitude and direction of these effects vary across different quantiles, underscoring how market conditions—such as high-demand phases—can amplify or dampen geopolitical shocks. These patterns highlight the vulnerability and complexity of global supply chains for critical minerals, mainly where supply is highly concentrated in geopolitically sensitive regions.

Based on our findings, policymakers and industry stakeholders must adopt a multi-faceted strategy to mitigate the adverse effects of geopolitical risk on energy transition minerals. KRLS and QR analyses reveal that minerals such as cobalt, nickel, rare earth, and graphite are particularly susceptible to negative impacts from heightened geopolitical uncertainty, so efforts should prioritize targeted supply diversification. This can be achieved by exploring new reserves and developing strategic partnerships in politically stable regions, thereby reducing overreliance on geopolitically sensitive areas. In parallel, flexible stockpiling measures, aligned with real-time risk assessments, are warranted; adaptive inventories can serve as buffers when QR estimates indicate amplified price volatility at higher quantiles. Additionally, enhancing domestic refining capacity and localized processing—in regions with stable political climates—can further fortify supply chains, particularly for those minerals exhibiting sharp negative responses.

Complementary to these supply-side strategies, risk-sensitive trade policies are recommended. These policies should include mechanisms such as conditional agreements and contingency clauses, which are designed to accommodate the nonlinear risk patterns identified in our analysis. Finally, proactive diplomatic engagement through resource-sharing agreements and multilateral initiatives can mitigate external shocks and stabilize mineral markets in an increasingly uncertain global environment. Collectively, these recommendations provide a robust framework to enhance resilience amidst ongoing geopolitical turbulence.