I. Introduction

The relationship between trade policy uncertainty (TPU) and energy-related uncertainty (ERU) is complex, as global trade and energy markets are deeply intertwined (Berdysheva & Ikonnikova, 2021). TPU, often driven by geopolitical tensions, trade policy shifts, or global supply chain disruptions, affects energy markets by influencing energy demand, supply logistics, and price stability (Wang & Wu, 2023). Tariffs or export restrictions on key energy resources, such as oil, gas, or coal, can disrupt global energy supply chains and create volatility in energy prices. These measures may also slow down energy investments and long-term contracts, as stakeholders might become reluctant to commit in an unpredictable environment.

ERU also could exacerbate TPU. For example, energy shocks—such as oil supply crises, natural gas shortages, or extreme fluctuations in energy prices—can ripple through economies, affecting production costs, competitiveness, and trade balances (Le & Chang, 2013). Nations highly dependent on energy imports are especially vulnerable, as their economic stability may be at the mercy of external energy market conditions. In response, some countries may adopt protectionist trade policies to secure their energy supplies, further intensifying trade tensions. Thus, the interplay between trade and energy uncertainty can create a cycle of volatility that poses risks to global economic stability and hinders coordinated responses to energy challenges, such as climate change mitigation and sustainable resource management.

China’s economy is heavily influenced by both trade and energy sectors, with domestic and international policies playing a critical role (Adebayo et al., 2022). The uncertainty surrounding trade policies, especially in the context of significant global events such as US-China relations, Brexit, and broader economic shifts, has introduced volatility into the energy sector (Olasehinde-Williams et al., 2023). While previous studies have primarily examined the impact of TPU on financial markets, limited research has been conducted on the dynamic interaction between TPU and ERU.

The theoretical foundation of this study is based on the work of Diebold and Yilmaz (2012), who developed a framework for measuring financial market spillovers that has since been extended to other economic variables (see Balcilar & Usman, 2021). Antonakakis and Gabauer (2017) further refined these measures to capture time-varying connectedness. Although past studies have demonstrated that trade policies can significantly impact energy prices and market stability, the specific relationship between TPU and ERU, particularly in an emerging economy like China, has not been thoroughly explored.

There remains a gap in the literature regarding the relationship between TPU and ERU in China, as previous studies have often considered these variables in isolation. This gap raises the critical question of how TPU and ERU interact dynamically in China and what the implications of this interaction are for economic stability. The motivation for this study is driven by the increasing complexity of global trade relations and energy markets, making it essential to understand this interconnectedness as China’s influence on the global economy continues to grow.

This study contributes to the literature in several ways. It provides a novel analysis of the bidirectional relationship between TPU and ERU in China, utilizing a TVP-VAR approach to capture dynamic interactions from February 2000 to October 2022. By focusing on China, this research adds valuable insights into the economic implications of policy uncertainty in emerging markets, offering new perspectives for policymakers and market participants.

II. Data and Methodology

A. Methodology

To analyze volatility spillovers between TPU and ERU in China, we employ the TVP-VAR connectedness approach developed by Gabauer and Gupta (2018). This method builds upon the connectedness framework introduced by Diebold and Yılmaz (2012) and enhanced by Antonakakis and Gabauer (2017). The approach is particularly advantageous as it enables the decomposition of shocks, revealing both international and domestic spillovers associated with uncertainties. Following Diebold and Yılmaz (2012), we specify a TVP-VAR model in which variances are allowed to evolve dynamically using a stochastic volatility Kalman Filter. The model is outlined as follows:

\[y_{t} = \beta_{t}z_{t - 1} + \varepsilon_{t}\ \ \varepsilon_{t}\left| F_{t - 1}\sim N\left( 0,S_{t} \right) \right. \tag{1}\]

\[{vec(\beta}_{t}) = vec(\beta_{t - 1}) + v_{t}\ \ v_{t}\left| F_{t - 1}\sim N\left( 0,R_{t} \right) \right.\tag{2}\]

Here, and represent the and dimensional vectors, respectively. represents the dimensional time-varying coefficient matrix. refers to the dimensional error disturbance vector. is the time-varying variance-covariance matrix. are dimensional vectors.

Next, we convert the VAR model into a vector moving average (VMA) form to calculate the generalized impulse response functions (GIRF) and the generalized forecast error variance decomposition (GFEVD), as proposed by Pesaran and Shin (1998) and Balcilar et al. (2024). Using GFEVD, we derive the total connectedness index (TCI) as follows:

\[\mathcal{C}_{\mathcal{t}}^{\mathcal{q}}\left( \mathcal{J} \right) = \frac{\sum_{\mathcal{i},\mathcal{j} = 1,\mathcal{i} \neq \mathcal{j}}^{\mathcal{N}}{\varnothing_{\mathcal{ij},\mathcal{t}}^{\mathcal{q}}\left( \mathcal{J} \right)}}{\mathcal{N}} \tag{3}\]

Note that is the generalized forecast error variance decomposition.

Specification for the case where TPU transmits its shock to ERU (total directional connectedness to others) is given thus:

\[\mathcal{C}_{\mathcal{i} \rightarrow \mathcal{j},\mathcal{t}}^{\mathcal{q}}\left( \mathcal{J} \right)\ = \frac{\sum_{\mathcal{j} = 1,\mathcal{i} \neq \mathcal{j}}^{\mathcal{N}}{\varnothing_{\mathcal{ji},\mathcal{t}}^{\mathcal{q}}\left( \mathcal{J} \right)}}{\sum_{\mathcal{j} = 1}^{\mathcal{N}}{\varnothing_{\mathcal{ji},\mathcal{t}}^{\mathcal{q}}\left( \mathcal{J} \right)}} \tag{4}\]

Specification for the case where TPU receives some shock from ERU (total directional connectedness from others) is given thus:

\[\mathcal{C}_{\mathcal{i} \leftarrow \mathcal{j},\mathcal{t}}^{\mathcal{q}}\left( \mathcal{J} \right) = \frac{\sum_{\mathcal{j} = 1,\mathcal{i} \neq \mathcal{j}}^{\mathcal{N}}{\varnothing_{\mathcal{ij},\mathcal{t}}^{\mathcal{q}}\left( \mathcal{J} \right)}}{\sum_{\mathcal{i} = 1}^{\mathcal{N}}{\varnothing_{\mathcal{ij},\mathcal{t}}^{\mathcal{q}}\left( \mathcal{J} \right)}} \tag{5}\]

B. Data

Monthly data on China’s TPU and ERU, spanning from February 2000 to October 2022, are used for the empirical analysis. The Trade Policy Uncertainty (TPU) index, developed by Davis et al. (2019), captures the degree of TPU in China. This index is derived from tracking how frequently Chinese newspapers mention economic uncertainty related to trade policy decisions. Meanwhile, the degree of Energy-Related Uncertainty (ERU) in China is measured using the index constructed by Dang et al. (2023), which is based on an analysis of country reports provided by the Economist Intelligence Unit.

The descriptive statistics for these variables are detailed in Table 1. TPU exhibits a notably higher variance compared to ERU, despite both variables having positive mean values. Additionally, both variables are positively skewed, indicating that most extreme uncertainty values lie to the right of the mean. The presence of excess kurtosis in both variables suggests fat tails in their distributions, reflecting more outliers than expected under a normal distribution. The statistically significant Jarque–Bera test results further confirm the non-normality of these variables.

The Elliott et al. (1996) unit root test results reveal that both variables are stationary. Moreover, the Ljung-Box serial correlation test results indicate the presence of autocorrelation in both datasets. This justifies the use of a TVP-VAR model with time-varying variances, as employed in this study.

III. Main Findings

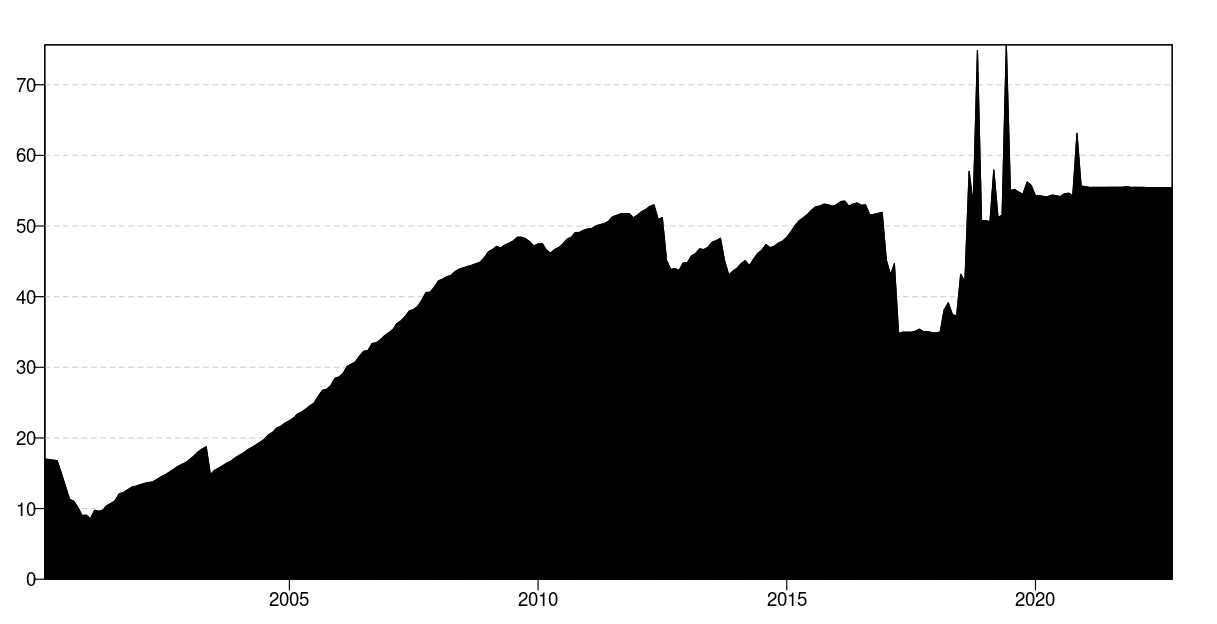

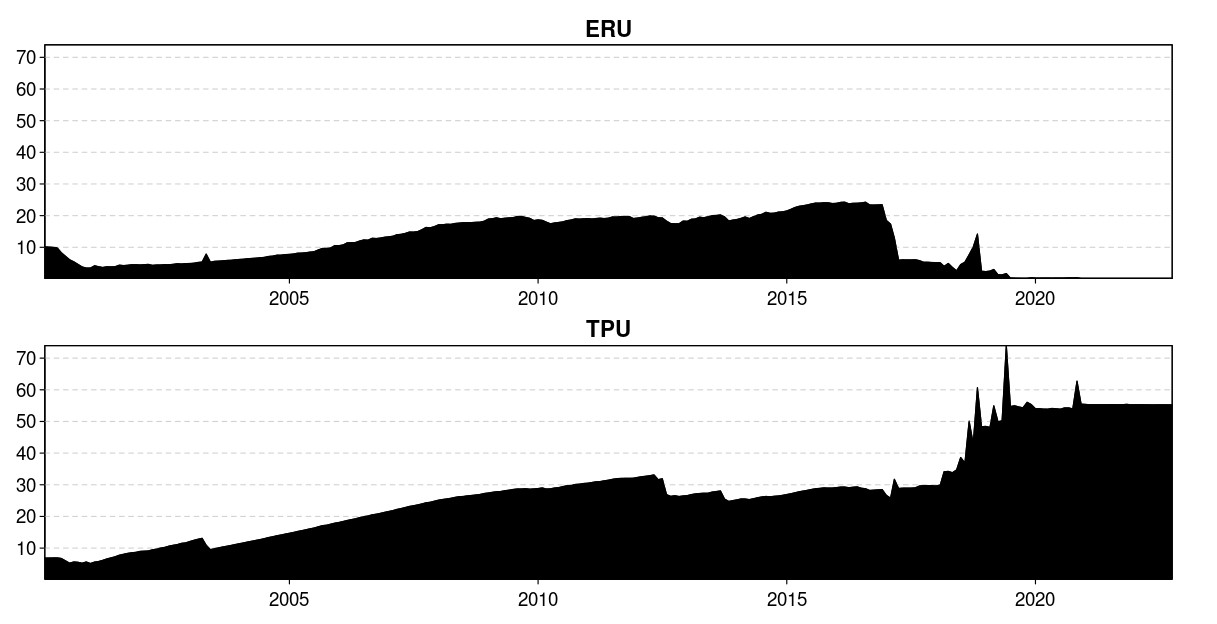

First, we report the average dynamic results that do not account for time-specific variations, as shown in Table 2. The Total Connectedness Index (TCI), which measures the overall interdependence or volatility spillovers among the variables, is calculated at 19.95. This indicates that, on average, the degree of connectedness between China’s Trade Policy Uncertainty (TPU) and Energy-Related Uncertainty (ERU) is approximately 20%. Furthermore, the analysis of the “TO” and “FROM” values reveals that ERU has the higher “FROM” value, while TPU exhibits the higher “TO” value. Additionally, the net directional connectedness values demonstrate that ERU serves as the primary risk receiver, whereas TPU acts as the primary risk transmitter.

Next, we present the findings derived from the TVP-VAR connectedness analysis. Several insights can be drawn from these results. The Total Connectedness Index displayed in Figure 1 underscores the time-varying nature of the system. The degree of connectedness between TPU and ERU closely reflects significant global events, including the global financial crisis, China’s leadership transition, the Eurozone crisis, Brexit, the Trump election, and US-China trade tensions. Moreover, the total directional connectedness to others, illustrated in Figure 2, further confirms the dynamic and time-varying interplay between these variables. The data clearly indicate that TPU is the primary net risk transmitter, while ERU functions as the net risk receiver.

Overall, the findings of this study reveal that there are significant, time-varying volatility spillovers between TPU and ERU in China. These results generally align with the claims of Karabulut et al. (2020), Qin et al. (2020), and Assaf et al. (2021).

IV. Conclusion

This study explores the dynamic relationship between TPU and ERU in China, an emerging economy where both trade and energy are integral to economic growth and stability. The results indicate that TPU acts as a significant transmitter of risk to ERU, particularly during periods of global economic instability. This dynamic connectedness suggests that policymakers must consider the broader implications of trade decisions, especially their potential to induce volatility in critical sectors like energy. As China continues to play a pivotal role in global trade and energy markets, understanding and managing the interplay between these uncertainties becomes crucial for sustaining economic growth and ensuring market stability.

To address the interconnectedness between TPU and ERU, China should develop integrated policy frameworks that align trade policies with energy strategies. Establishing an inter-ministerial task force that includes representatives from trade, energy, and finance ministries will ensure cohesive policymaking and regular assessments of how proposed trade policies might impact energy markets. Additionally, implementing advanced monitoring systems that track TPU and ERU in real-time using big data analytics and predictive models can provide early warnings of potential disruptions, enabling proactive policy adjustments.

China should also prioritize the diversification of its energy mix, with a stronger focus on renewable energy sources, to reduce the energy sector’s vulnerability to trade policy fluctuations. This can be achieved by increasing investments in renewable energy infrastructure and incentivizing private sector participation through subsidies, tax breaks, and public-private partnerships. Moreover, encouraging businesses, particularly in the energy sector, to adopt comprehensive risk management strategies such as the use of financial instruments like hedging contracts and insurance products can help mitigate the impacts of TPU-induced market volatility. Finally, strengthening international cooperation through multilateral negotiations and active participation in global forums focused on energy security and trade stability will further reduce the adverse effects of TPU on global energy markets, promoting economic resilience and sustainable growth.

It is important to mention that while the findings from this study are useful for drawing conclusions on the relationship between TPU and ERU, certain limitations still exist. One is that the study did not control for possible confounding variables that may influence the relationship between TPU and ERU. As such, future related studies may further test the relationship while controlling for possible confounding effects. Another limitation is that the uniqueness of China’s economy means that the inferences made may not be completely generalizable, especially when considering other large economies. Extending this study to other regions with differing characteristics is thus suggested as another direction for future research.