I. Introduction

Nigeria’s economy has benefited from petrol subsidies since the 1970s, with the government selling petrol to citizens below the market-determined price. However, calls for removing the subsidy grew due to transparency and corruption issues in the economy. Critics have argued that the subsidy consumed a significant portion of government revenue, with over N4.39 trillion ($9.7 billion)[1] spent on it in 2022. Despite this, some contended that subsidies were a way for ordinary Nigerians to benefit from the government, given the high demand for energy amidst the country’s energy challenges. In May 2023, the Nigerian government completely removed subsidies on petrol and later floated the exchange rate. Consequently, this led to multiple economic challenges, including contracted growth and increased inflation due to the country’s heavy dependence on imported refined petrol.

Empirical evidence indicates that large positive oil price shocks can lead to persistent inflationary pressures (Ali Ahmed & Wadud, 2011; Berument et al., 2010; Choi et al., 2018; Ju et al., 2016; Maheu et al., 2020; Salisu et al., 2017; Tule et al., 2020; Vatsa & Mixon, 2022). In line with this, Salisu et al. (2017) pointed out that oil price dynamics are more significant for exporting countries than for importing ones. One way to address this challenge is through macroeconomic fiscal and monetary policies. Fiscal policies involve using taxation and spending strategies to stabilize the economy against shocks such as energy price hikes. On the other hand, monetary policies aim to stabilize the macroeconomy (output and inflation) by influencing liquidity and adjusting interest rates. For example, Kure and Salisu (2024) noted that inflation can be driven by both demand and supply-side factors and coordinated fiscal and monetary policy can be effective tools for stabilization. In addition, effective coordination between fiscal and monetary policies ensures that measures taken by one policy do not counteract the other (Šehović, 2013). Studies such as Azad et al. (2021), De Grauwe & Foresti (2023), Dosi et al. (2015), Hallett et al. (2011), and Leeper & Zhou (2021) have highlighted the effectiveness of policy coordination in restoring macroeconomic stability. Although an optimal policy mix is desired, there is often a conflict between the two policies. De Grauwe and Foresti (2023) pointed out that fiscal dominance often undermines the effectiveness and credibility of central banks. However, Büyükbaşaran et al. (2020) note that monetary and fiscal shocks respond to demand and supply shocks, and the nature of these shocks is important. Similarly, Lambertini and Rovelli (2003) observe that the nature of shocks influences the interaction between the two policies.

In light of the foregoing, this study seeks to determine how monetary and fiscal policy coordination can be used to mitigate the effects of energy price shocks on output and inflation in Nigeria. To achieve this objective, this study raises two empirical questions: First, what are the empirical effects of energy shocks on output and inflation in Nigeria? Secondly, what is the best fiscal-monetary policy mix for managing the effect of energy price shocks on output and inflation in Nigeria? This study differs from extant studies in application of the Bayesian Vector Autoregressive model identified with sign-and-zero restriction (SZR-BVAR) to simulate the effects of various fiscal and monetary policy mixes on inflation and growth responses to energy price shocks especially in Nigeria.

II. Method and data

A. Theoretical and methodical framework

This study relies on the New Keynesian model that advocates the use of fiscal and monetary tools to stabilize the economy during shocks, say, persistent energy price hikes. Moreover, energy prices are important sources of shocks, especially in oil-exporting countries, that are highly vulnerable to fluctuations (Salisu et al., 2017). In addition, large and persistent increases in energy prices can cause a leftward shift in the aggregate supply curve, leading to a reduction in production (output) and price increases due to rising marginal costs. This prediction can explain Nigeria’s ongoing experience following the complete removal of subsidies on petrol products. Thus, this study suggests that coordinated fiscal and monetary policy can be a potent tool for mitigating the adverse effects of persistent energy price shocks on inflation and output growth in Nigeria. This study uses a Bayesian Vector Autoregressive model identified with sign-and-zero restriction (SZR-BVAR) to simulate the effects of various fiscal and monetary policy mixes on inflation and growth responses to energy price shocks. In doing so, the question “What is the optimal fiscal-monetary policy response for mitigating the adverse effects of energy price shock on inflation and economic growth?” is addressed. In addition, the zero-and-sign restriction identification strategy provides this study with a suitable framework to capture the complex dynamics of fiscal-monetary policy interaction conveniently. This study follows the lead of Kamber et al. (2016) to specify the VAR model as follows:

\[\alpha_{0}X_{t} = \sum_{i = 1}^{p}{\alpha_{i}X_{t - i}} + \mu_{t}\tag{1}\]

where:

\[X_{t} = \lbrack pms_{t}\text{, gre}\text{v}_{t},\text{ gex}\text{p}_{t},mp_{t},exr_{t},rgdp_{t}\text{,in}\text{f}_{t}\rbrack^{\mathstrut'} \tag{2}\]

In Equation (2), is a vector of premium motor spirit government revenue government expenditure monetary policy exchange rate real growth and inflation The structural shocks in Equation (1) are assumed to be independent. All the variables are in logarithmic form except growth, monetary policy, and inflation which are in percentages. Two lags were used in the estimation of Equation (2) and it satisfies the stability condition. This study proxied monetary policy with the treasury bills rate and energy price with PMS price. Equation (1) is estimated with quarterly data from 2010Q1 to 2022Q4. This study obtained government revenue, expenditure, treasury bills, inflation, and GDP data from the CBN statistical bulletin and PMS price from the National Bureau of Statistics. The data on nominal effective exchange were obtained from the IMF Statistics. In addition, the sign restrictions on the impulse responses of fiscal and monetary policy in the first two quarters following a shock to energy prices are represented in Table 1.

The first row of Table 1 applies sign restrictions to identify a scenario where fiscal and monetary authorities respond to energy prices with an expansionary fiscal and contractionary monetary policy mix. The first column shows the shock and its policy mix response (i.e., deficit-tightening policy mix in response to energy price shock). For example, increases in energy prices (positive shock) are represented by a positive sign (“+”); the fiscal deficit is represented by a decline (“-”) in government revenue (GRev) and an increase (“+”) in government expenditure (GExp). The monetary tightening is represented by an increase “+” in the monetary policy rate (MP). The responses of exchange rate (Exr), output (Growth) and inflation are unrestricted (ur). The remaining three fiscal-monetary policy mixes (Deficit & Easing, Surplus & Tightening, and Surplus & Easing) are similarly identified using signs restrictions.

III. Results

Table 2 and Figure 1 present empirical estimates from the SZR-BVAR results, showing the impact of fiscal and monetary policy responses to a 1% shock to energy prices on growth and inflation. From the baseline estimate in Table 2, a 1% positive shock to energy prices reduces growth by 0.24% and increases inflation by 1.01%. However, when there is a mixture of contractionary fiscal and expansionary monetary policy responses, a 1% positive shock to energy prices increases growth by 0.12% and inflation by 0.23%.

The estimates also indicate that a 1% positive shock to energy prices increases growth by 1.6% and decreases inflation by 1.81% when both fiscal and monetary policies are contractionary. Conversely, a 1% increase in energy prices under expansionary fiscal and monetary policies results in a 1.75% decline in growth and a 3.63% increase in inflation. Finally, a 1% rise in energy prices under expansionary fiscal and contractionary monetary policies decreases economic growth by 2.16% and increases inflation by 2.49%.

These results suggest that a simultaneous mix of contractionary fiscal and monetary policies in response to a surge in energy prices would expand economic growth and reduce inflationary pressures. This scenario is plausible because persistent deficit spending by the government may crowd out private investment, leading to a contraction in overall economic activity, while loose monetary policy can create excess liquidity chasing few goods, generating demand-side inflationary pressures.

In summary, the estimates reported in Table 2 suggest that fiscal expansion, coupled with either contractionary or expansionary monetary policies in response to energy price shocks, dampens economic growth and increases inflationary pressures. This result may reflect fiscal dominance and lend support to Woodford’s (1994) fiscal principle of price level, indicating that fiscal discipline is essential for maintaining growth and price stability in Nigeria. Moreover, the estimates suggest that contractionary fiscal policy combined with monetary tightening significantly reduces inflation and stabilizes economic growth. This finding implies that the optimal policy combination for mitigating the impact of energy price shocks on inflation and output is contractionary fiscal policy complemented either with monetary contraction or expansion.

Figure 1 shows the response of inflation to a 1% increase in energy prices under four policy scenarios. The impact of an energy price shock on inflation produces the optimal reduction when contractionary fiscal policy is combined with contractionary monetary policy. This means that tightening liquidity, with some short-term easing from the monetary side as indicated by the red line, can help moderate inflationary pressures from energy price shocks. However, Figure 1 demonstrates that expansionary fiscal policy combined with either monetary expansion or contraction in response to energy shocks produces the highest increase in inflation. This mixture of fiscal and monetary policy amplifies inflationary pressures in Nigeria, consistent with the fiscal theory of the price level. Overall, this policy mixture suggests that tightening money is the optimal option for managing the impact of energy price shocks on inflation in Nigeria.

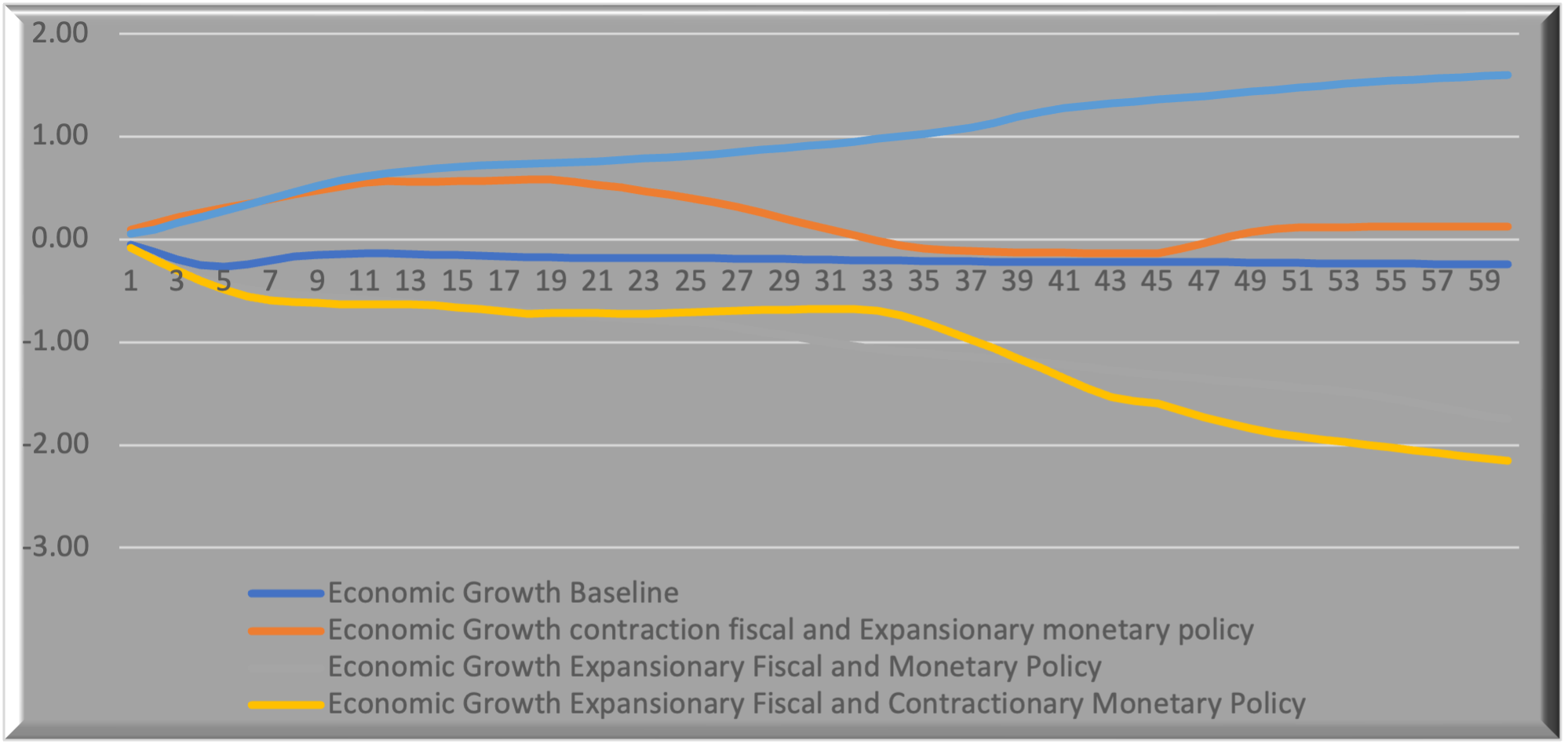

Figure 2 illustrates the response of economic growth to a 1% increase in energy prices under four policy scenarios. It shows that the highest levels of economic growth occur when both contractionary fiscal and monetary policies are implemented together, suggesting that tightening liquidity can help mitigate the impact of energy price shocks and promote economic growth in Nigeria.

IV. Conclusion

The estimates from the SZR-BVAR indicate that fiscal and monetary policy responses to shock in energy prices have significant and persistent impacts on growth and inflation in Nigeria. Specifically, a positive shock to energy prices reduces economic growth and increases inflation but the effects depend on the mixture of fiscal and monetary policies. However, the mixture of contractionary fiscal and monetary policies appears to be the optimal combination for mitigating inflationary pressures while promoting economic growth. On the other hand, expansionary fiscal policies, whether combined with contractionary or expansionary monetary policies, tend to exacerbate inflation and hinder growth. These results underscore the importance of a coordinated policy in managing the impacts of energy price shocks. The evidence suggests that maintaining fiscal discipline and coordinated fiscal and monetary policies can effectively stabilize growth and inflation.

Acknowledgment

The article has been prepared with the support of the Ministry of Science and Higher Education of the Russian Federation (Ural Federal University Program of Development within the Priority-2030 Program)