1. Introduction

The objective of this paper is to investigate the role of pandemics in the fluctuations of oil prices (OP). The outbreak of the coronavirus disease (COVID-19) in 2019-2020 resulted in a large-scale economic shutdown, hindering not only economic growth but also reducing the demand for oil. Further, with international travel banned, tourism activity has been restricted, thus reducing the demand for oil. . The net effect was a substantial decline in OP in the first quarter of 2020: OP fell by as much as 80%We, therefore, infer that pandemics do influence the oil market. A similar effect on oil price was observed during the severe acute respiratory syndrome (SARS) in 2003.

However, this often-held negative relation between OP and pandemics may not always hold. Oil demand and pandemics may also share a positive relation, as observed during the time of the bird flu (H5N1) in 2006. Another possibility is that pandemics that occur in oil-producing countries may reduce their oil supply, thus driving up OP . It is also possible that the correlation between pandemics and OP may be influenced by economic or geopolitical factors (Su et al., 2017; Su, Khan, et al., 2019). The swine flu (H1N1) from 2009 to 2010, for instance, could not affect OP significantly. One reason for this outcome could be because OP fluctuates with the U.S. dollar and the global economic situation. Generally, the interaction between pandemics and OP is complicated, and this paper investigates this relation to confirm what precisely is the relationship.

We acknowledge that there are a few studies that explore the interrelationship between pandemics and the oil market. Flynn et al. (2012) point out that the onshore oil operations increase human incursions into wildlife areas, promoting mechanisms for potential zoonotic pathogen transmission which may cause pandemics to occur. Sharif et al. (2020) suggest that there are certain influences from the COVID-19 and OP to geopolitical risks, economic policy uncertainty and the U.S. stock market. Wang et al. (2020) indicate that COVID-19 has a significant effect on the cross-correlation of multifractal property between oil and several agricultural futures markets. It follows that the literature to-date presents a one-way impact of pandemics on the oil market. Our study adds to this literature and the novelty is that we employ a quantitative indicator to measure the pandemics rather than dummy variables or relying only qualitative analysis. A limitation of existing studies is that they cannot take into account the time-varying parameters in the empirical models. We address this issue by applying the bootstrap sub-sample rolling-window causality test (Su, Wang, et al., 2019) to investigate the non-constant correlation between global pandemics and the oil market.

The remainder of the paper is as follows: Section 2 explains the theoretical model. Section 3 describes the empirical methods. Section 4 introduces the data. Section 5 reveals the empirical outcomes. Section 6 summarizes the results.

2. Intertemporal capital asset pricing model

We employ the intertemporal capital asset pricing model (ICAPM), developed by Cifarelli and Paladino (2010) to analyze the transmission mechanism between pandemics and OP. Assuming that there are two kinds of investors (informed and feedback investors) in the oil market, and the systematic risk is the occurrences of pandemics captured by the pandemics index (PDI). Informed investors consider the risk-return when they invest, while feedback investors take the serial correlation of OP into account. The informed investors’ demand for oil can be written as Equation (1):

\[i_{t}^{D} = \ \frac{E_{t - 1}\left( \text{OP}_{t} \right) - \text{OP}^{f}}{\mu(\text{PDI}_{t)}}\hspace{25mm}(1)\]

where is the share of oil stored by the informed investors; is a monotonically increasing function; is without is the conditional expectation of The share of oil invested by the feedback investors is where Then, Equation (1) can be transformed to Equation (2) as:

\[E_{t - 1}\left( \text{OP}_{t} \right) = \text{OP}^{f} + \mu\left( \text{PDI}_{t} \right) - \theta\mu(\text{PDI}_{t})\text{OP}_{t - 1}\hspace{5mm}(2)\]

Obviously, the coefficient of is a positive value as Thus, high may lead to increase, in order to compensate for the losses caused by pandemics. Also, we can obtain a hypothesis from the ICAPM, that is can be positively influenced by

3. Methodology

To test our hypothesis, his paper applies the residual-based bootstrap (RB)-based modified-likelihood ratio (LR) statistics (Shukur & Mantalos, 1997, 2000). Based on this method, we can obtain the correlation between PDI and OP, but this relationship may be affected by the U.S. dollars (USD) since is denominated in USD (Su et al., 2020). Thus, we select the USD index (USDX) as a control variable in the VAR system as Equation (3):

\[\begin{bmatrix} \text{PDI}_{t} \\ \text{OP}_{t} \\ \end{bmatrix} = \begin{bmatrix} \gamma_{10} \\ \gamma_{20} \\ \end{bmatrix} + \begin{bmatrix} \gamma_{11}(L) & \gamma_{12}(L) & \gamma_{13}(L) \\ \gamma_{21}(L) & \gamma_{22}(L) & \gamma_{23}(L) \\ \end{bmatrix}\begin{bmatrix} \text{PDI}_{t} \\ \text{OP}_{t} \\ \text{USDX}_{t} \\ \end{bmatrix} + \begin{bmatrix} \mu_{1t} \\ \mu_{2t} \\ \end{bmatrix} \hspace{5mm}(3)\]

where is a white-noise process. where i=1, 2; j=1, 2, 3; p is an optimal lag order, and we select p=1 based on the Schwarz Information Criterion (SIC); L is a lag operator, and there is The null hypothesis that OP cannot impact PDI, that is can be accepted when does not Granger cause and vice versa. Also, the null hypothesis that has no effect on can be accepted in a similar way.

However, this full-sample test ignores the time-varying interrelation between and therefore, we perform the Sup-F, Ave-F, Exp-F and Lc tests[1] to examine the parameter stability (Hansen, 1992). If there exists parameter instability, we should employ the bootstrap sub-sample rolling-window causality test to explore the time-varying interaction between and This sub-sample method (Balcilar et al., 2010) separates the whole sample into small sections based on the rolling-window width. Each small section can obtain an outcome from the full-sample test, then the results of the sub-sample test can be acquired. and are the averages of the entire estimations, revealing the effect from to and the influence of to respectively. In this relation, is the number of times of bootstrap iterations; and and are the estimations from Equation (3). Additionally, the choice of the rolling-window width cannot be less than 20 in the sub-sample test (Pesaran & Timmermann, 2005); we, thereby, select 24-months[2] to ensure the robustness of the empirical results (Su, Qin, et al., 2019).

4. Data

We choose the quarterly data from 1996:Q1 to 2020:Q1[3], to explore the relationship between the pandemics and oil market. During this period, there are several pandemic diseases around the world, such as the bird flu (H5N1) in 1998, the SARS in 2003, the H1N1 from 2009 to 2010, the Middle East respiratory syndrome (MERS) from 2014 to 2016, and COVID-19 in 2020. Given this, we choose the [4], developed by Ahir et al. (2018)[5], to reflect the severity of global pandemic diseases. Moreover, the price of crude oil has fluctuated rapidly during this period, which maybe partly caused by the occurrence of pandemics (e.g., COVID-19 in 2020). We choose the West Texas Intermediate crude oil price, our proxy for [6] to explore the potential interrelationship between PDI and OP. Moreover, we select the USDX[7] as a control variable in Equation (3), since USDX may influence the interaction between these two variables. In order to prevent the potential heteroscedasticity and possible instability, we take the natural logarithms and first differences of PDI, OP and USDX.

5. Empirical results

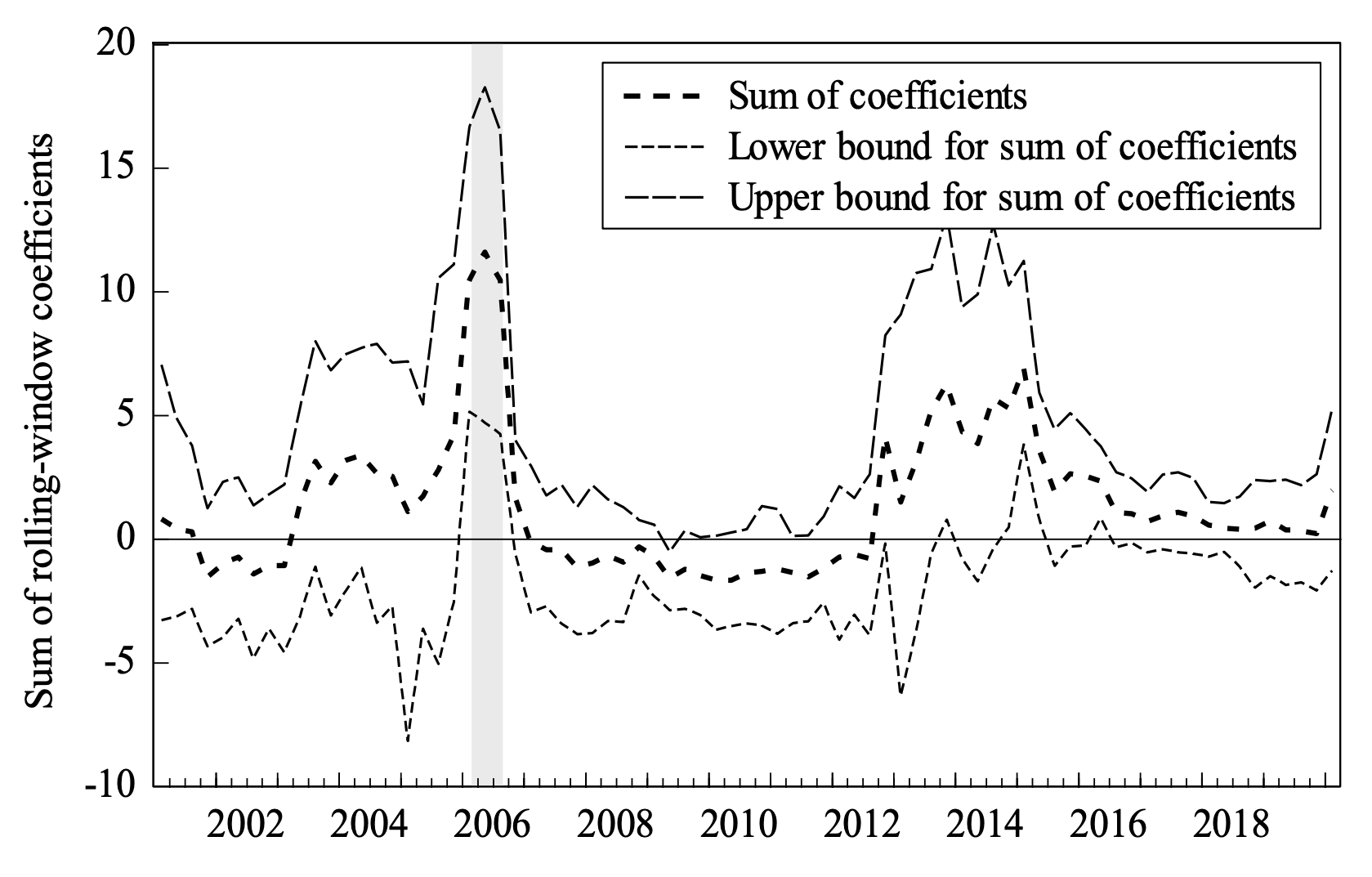

According to the Equation (3), the results of the full-sample causality between PDI and OP are shown in Table 1. There is no significant interrelationship between PDI and OP, which is inconsistent with ICAPM and the existing studies. However, the whole sample only has one-time Granger causality, which may not be ideal if there are non-stable parameters in the VAR system. We, therefore, perform parameter stability tests, and these results are revealed in Table 1. We can observe that PDI, OP and the VAR system parameters are non-constant. Thus, the mutual influence between PDI and OP is time-varying, and we explore it by employing the sub-sample test.

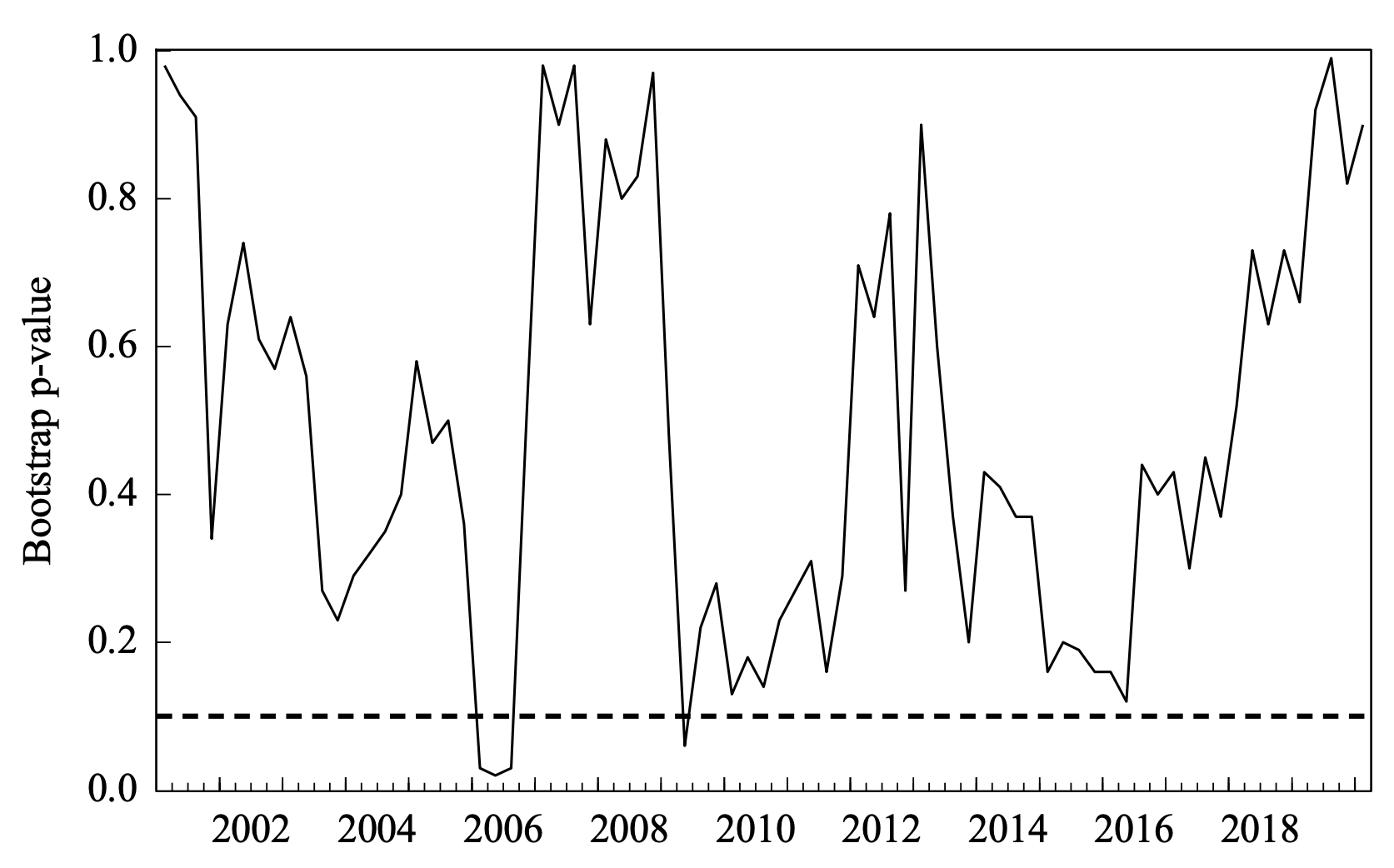

Figures 1 and 2 highlight the p-values and the effects of on has a negative influences on during the periods of 2003:Q1-2003:Q2, 2014:Q4-2015:Q2 and 2019:Q3-2020:Q1 at the 10% level.

The outbreak of SARS in 2003 has spread to the world. As of August 16, 2003, the cumulative number of patients worldwide was 8,422 and the death toll stood at 919. Thus, this global infectious disease causes to increase sharply during the period of 2003:Q1-2003:Q2. Although the Iraq war curtailed the oil supply, which resulted in a higher in 2003:Q1, there are two ways to explain the negative influence from on On the one hand, affected by SARS, the World Health Organization (WHO) had issued travel warnings or restrictions to many countries, especially to China. This move dramatically impacted the global tourism industry, causing the demand for civil aviation to decline. Thereby, the demand for aviation kerosene falls sharply, leading to decrease. On the other hand, high reduces public confidence, and the global economy slows down (e.g., massive unemployment and shutdown in some areas). As an indispensable raw material for industrial production, the demand for oil has dropped significantly which causes to further decline. Therefore, we can evidence that PDI can negatively influence during the period of 2003:Q1-2003:Q2.

In 2014, MERS has exploded on a large scale in West Africa, and the WHO had announced its end on January 14, 2016. This epidemic claimed more than 11,300 lives and infected more than 28,500 people; therefore, has been at a high level during this period. Then, we can explain the negative effect of to from three aspects. Firstly, the shocks on tourism (especially in Liberia, Sierra Leone and Guinea) reduced the demand for civil aviation and aviation kerosene, causing to decrease. Secondly, the economic downturn, caused by this pandemic disease, leads to a fall in oil demand and Thirdly, high in several oil-producing countries (e.g., Nigeria) may cut the oil supply, but the sharp increase in U.S. shale oil production has caused to continue to decline. Moreover, after the U.S. officially withdrew from quantitative easing (QE), the USD strengthened which intensified the decline in

The U.S. has experienced the outbreak of the influenza B virus in 2019, which at that time was the worst one recorded in the past four decades. Also, the COVID-19 spread to more than 200 countries or regions. Thus, increases sharply during the period with these pandemics. High causes a downturn in the tourism industry and the global economy, which in turn leads to a decline in Furthermore, COVID-19 pandemic has created public panic, and investors are more willing to store hedging assets. However, has been at a low level, decreasing the investors’ demand for oil and its related products to invest, which further reduces In addition, the global trade wars and the collapse of the Production Reduction Agreement exacerbate the plunge in Thereby, we infer that can be negatively affected by during the period of 2019:Q3-2020:Q1. These negative influences are not supported by the ICAPM, which indicates that high may cause to increase to compensate for the losses.

Figures 3 and 4 show the p-values and the effects of on positively affects during the period of 2006:Q1-2006:Q3 at the 10% level. The rise in during this period can be explained as follows. Firstly, the hype of investment funds has increased the demand for oil and its related products. Secondly, the geopolitical tensions (e.g., Iranian nuclear issue) have increased, and the oil production facilities in Nigeria have been attacked, both of them resulted in a decline in oil supply. Also, the bird flu (H5N1) occurred in several countries, such as Vietnam, Indonesia, China, Turkey, Greece, the Ukraine and Italy, which drove during this period. However, the rise in OP may increase the production costs, which weakens the prevention and control of this pandemic, causing to be at a relatively high level. Moreover, this epidemic does not have a similar shock on oil demand as COVID-19, thus, and move in the same direction during the period of 2006:Q1-2006:Q3. Thereby, oil market should be taken into account when analyzing the epidemic/pandemic situation.

6. Conclusion

This paper investigates the relationship between global pandemics and the oil market. The empirical results indicate that there is a negative influence from PDI to OP, which is inconsistent with the ICAPM. The main reason is that the pandemics may dramatically reduce the demand for oil and its related products because they slowdown the economy. Conversely, high OP may hinder the decline in PDI, which indicates a positive effect. Understanding the interrelationship between PDI and OP can provide lessons for investors. Investors can predict the trend of OP by considering PDI, allowing them to diversify their investments (change portfolios) and reduce risks. These aspects of investor behavior require more research.

The null hypothesis of the Sup-F test is that the parameters have no sudden structural change. The null hypothesis of the Ave-F and Exp-F tests is that the parameters cannot gradually change over time. The null hypothesis of the Lc test is that the parameters in the VAR system follow a random walk process.

To test the robustness of the sub-sample outcomes, we select the widths of 20-, 28- and 32- months to conduct the analysis, and the outcomes are unanimous with 24-months.

We use Q1, Q2, Q3 and Q4 to represent the first, second, third and fourth quarter, respectively.

The discussion about pandemic index is taken from the Economic Policy Uncertainty Database

(https://worlduncertaintyindex.com/data/).They search for the following keywords in the Economist Intelligence Unit country reports: Severe Acute Respiratory Syndrome, SARS, Avian flu, H5N1, Swine flu, H1N1, Middle East respiratory syndrome, MERS, Bird flu, Ebola, Coronavirus, Covid-19, Influenza, H1V1, and the World Health Organisation. Also, this index is a simple average for 143 countries.

The West Texas Intermediate (WTI) crude oil price is taken from the Energy Information Administration (https://www.eia.gov/dnav/pet/pet_pri_spt_s1_m.htm).

The U.S. dollar index is taken from the Federal Reserve Board (https://www.federalreserve.gov/econres/notes/ ifdp-notes/IFDP_ Note_Data_Appendix.xlsx).