I. Introduction

Crude oil is one of the globally traded commodities that constitutes a significant proportion of the global trade flows of oil-exporting countries. One of these countries, Nigeria, relies heavily on crude oil, which accounts for about 90 percent of its total exports (Oduyemi & Owoeye, 2020). Due to this, shocks in oil demand and supply affect the country’s macroeconomic indicators, including its exchange rates. Theoretically, an increase in crude oil demand causes the exchange rates of an oil-exporting country like Nigeria to appreciate, while its oil-importing counterparts experience currency depreciation. On the other hand, Fasanya et al. (2022) assert that currency fluctuations also trigger exchange rate influences on oil prices, causing shocks to oil demand and supply. This two-sided assertion has been corroborated by existing findings on the bidirectional relationship between oil shocks and exchange rates (see Umar & Bossman, 2023; Wang & Xu, 2022).

The relationship between global oil shocks and Nigerian exchange rates reveals significant vulnerabilities within the country’s macroeconomic framework. As a leading oil exporter, Nigeria would typically be expected to experience currency appreciation with rising crude oil prices. However, the opposite has occurred, with the Nigerian naira consistently depreciating. This ongoing depreciation is rooted in several structural challenges, including the mismanagement of oil wealth, the lack of functional refineries, and widespread economic misallocation. These issues have left the Nigerian economy highly susceptible to both internal and external crises, further weakening its currency. Moreover, inconsistent exchange rate policies, such as the persistent devaluation of naira since the Structural Adjustment Programme (SAP) in 1986 has exacerbated the issue, steadily eroding the currency’s value.

Despite evidence of bidirectional causality between oil shocks and exchange rates, empirical studies focusing on the Nigerian economy have partly examined the one-way directional effect of oil price shocks on exchange rate performance (see Ayinde et al., 2023; Fasanya et al., 2022). Although Maku et al. (2021) explore the bidirectional causality in Nigeria, this finding is limited to the oil price-exchange rate nexus. Considering this limitation, we conjecture the possible bidirectional interdependence between oil shocks and the Nigerian exchange rate using the four oil shock datasets by Baumeister & Hamilton (2019). Furthermore, we employ the wavelet coherence technique to investigate the time-and-frequency domain relationship between global oil shocks and Nigerian exchange rates to study how interdependence evolves over different global economic events.

The remainder of the is organized as follows. Section II discusses the methodology; Section III presents a discussion of empirical findings, and Section IV concludes the paper.

II. Methodology

A. Data and sources

We employed monthly time series data from February 1981 to December 2022. The Nigerian exchange rate per unit of the US dollar is gathered from the Central Bank of Nigeria (CBN), while the four oil shock datasets - covering oil supply shocks (OISS), economic activity shocks (ECAS), oil consumption demand shocks (OICDS), and oil inventory demand shocks (OIIDS) - are developed by Baumeister & Hamilton (2019) and sourced from the open-access website of Professor Christiane Baumeister (https://sites.google.com/site/cjsbaumeister/datasets?auth user=0). For the empirical analysis, we compute the Nigerian exchange rate returns as the percentage of log difference of official exchange rates: where and are current and previous month’s values of official exchange rates, respectively. We used the oil shock series based on the structural shocks computed and obtained directly from the aforementioned source.

Table 1 reports the summary statistics. The mean of exchange rate return is 1.338, suggesting that the holding naira yields appropriately 1 naira between February 1981 and December 2022. In contrast, the means of the oil shock dataset are negative, implying that the global economy experienced, on average, negative oil shocks during the period under consideration. The standard deviations of all the series are relatively low, except for exchange rate returns. The skewness and kurtosis statistics conform only to the standard thresholds of approximately 0 and 3, respectively, for oil inventory demand shocks, while the other dataset suggests evidence of non-normal distribution.

B. Estimation technique

This study applies the wavelet coherence technique to examine the interdependency between global oil shocks and Nigerian exchange rates. Aside from explaining the bidirectional interdependence between the two variables, wavelet coherence is suitable for investigating the evolution of the relationship between the variables over time and frequency spectra (Badmus et al., 2023). We begin the specification, following Torrence & Compo (1998), by specifying the cross-wavelet transform and cross-wavelet power models to explain the sequence of variation between each oil shock and the Nigeria exchange rates as follows:

\[M_{pq}(b,d) = M_{p}(b,d)M_{q}^{\#}(b,d)\tag{1}\]

From Equation (1), the two continuous wavelet transforms of and are denoted by and respectively; and and denote the measure and is the combined conjugate. Furthermore, denotes the cross-wavelet transforms that generate the cross-wavelet power. This transformation allows the estimation to be decomposed into time and frequency domains, with the time phase illustrating the progression of the time series sequence at each measurement point. Additionally, the relationship between the variables is examined using wavelet coherence within both the time and frequency dimensions by calculating the adjusted wavelet coherence coefficient, as proposed by Torrence & Webster (1999) and modified by Afshan et al. (2018), as follows:

\[\small{H^{2}(b,d) = \frac{\left| N\left( N^{- 1}M_{pq}(b,d) \right) \right|^{2}}{N\left( N^{- 1}\left| M_{p}(b,d) \right|^{2} \right)N\left( N^{- 1}\left| M_{q}(b,d) \right|^{2} \right)}}\tag{2}\]

where (b, d) represents the smoothing operator (S), and ranges between 0 and 1. When is less than 0.5, it signifies a weak correlation, illustrated by blue colors. Conversely, when is 0.5 or greater, it indicates a strong correlation, depicted by yellow or red colors.

III. Empirical Results

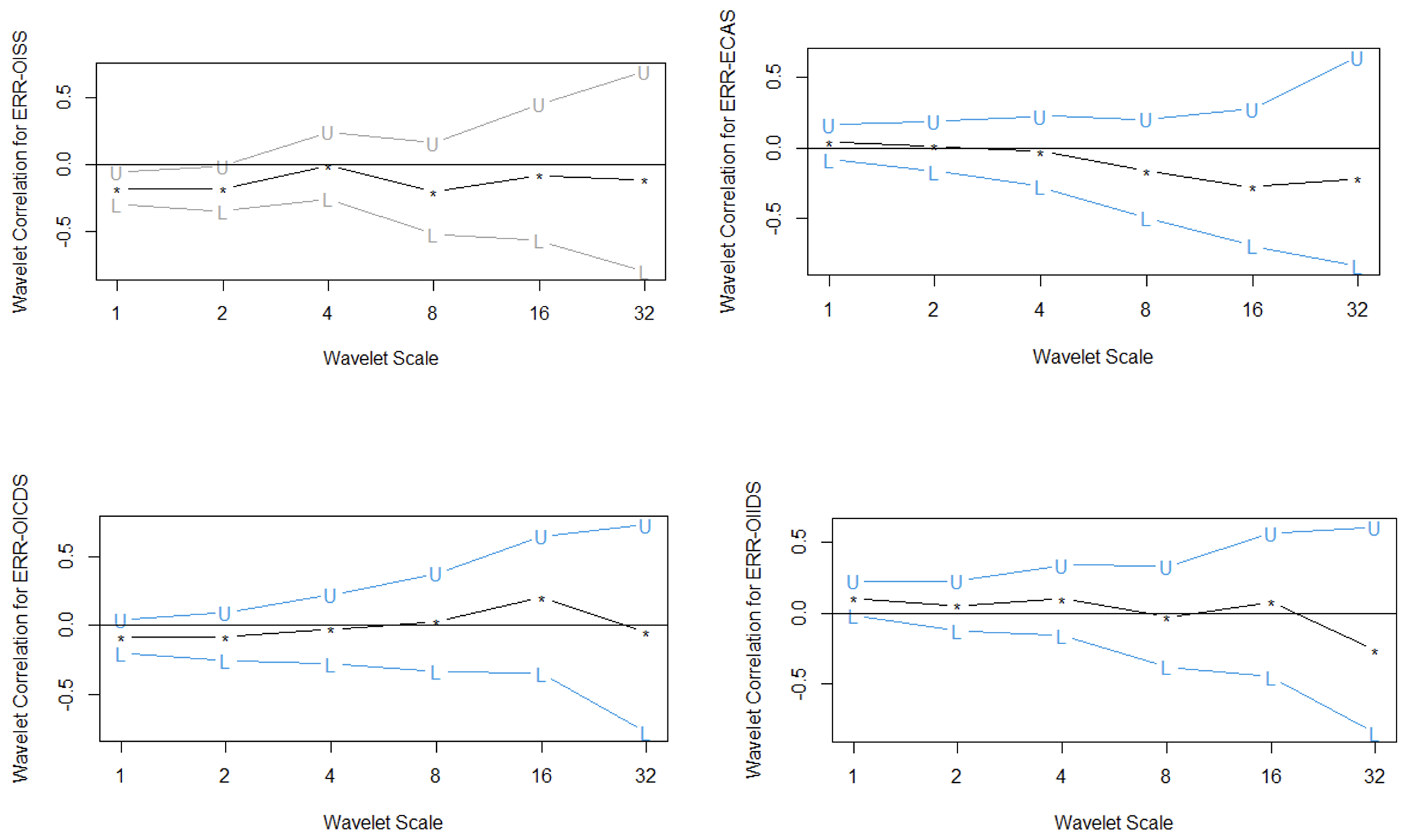

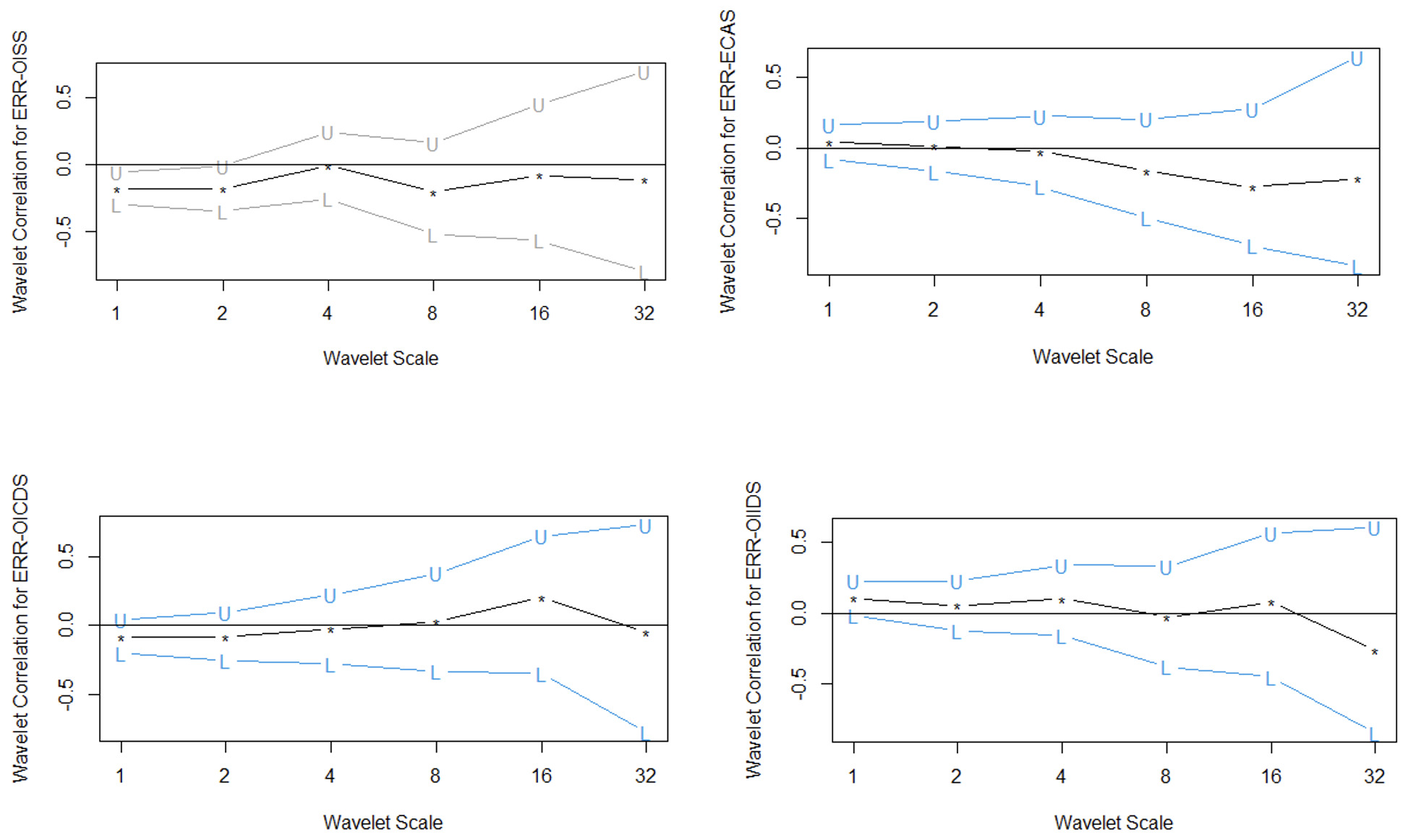

The discussion of the empirical results begins with the wavelet correlation plots of oil shocks and Nigerian exchange rates over different wavelet scales, as reported in Figure 1. The correlation between Nigerian exchange rate returns and oil shock measures is not consistent across different periods. While there is a negative correlation between oil supply shocks and exchange rate returns as well as between oil consumption demand shocks and exchange rate returns in the short run, the opposite is true for economic activity shocks and oil inventory demand shocks with exchange rate returns. However, there is evidence of a negative correlation between exchange rate returns and all the measures of oil shocks in the very long-run period, except for ERR-OICDS, which has a positive correlation in the long-run and very long-run. This implies a heterogeneous correlation between exchange rate returns and oil shock indicators across different wavelet scales, with prominent negative relationships in the long-run horizon except for OICDS.

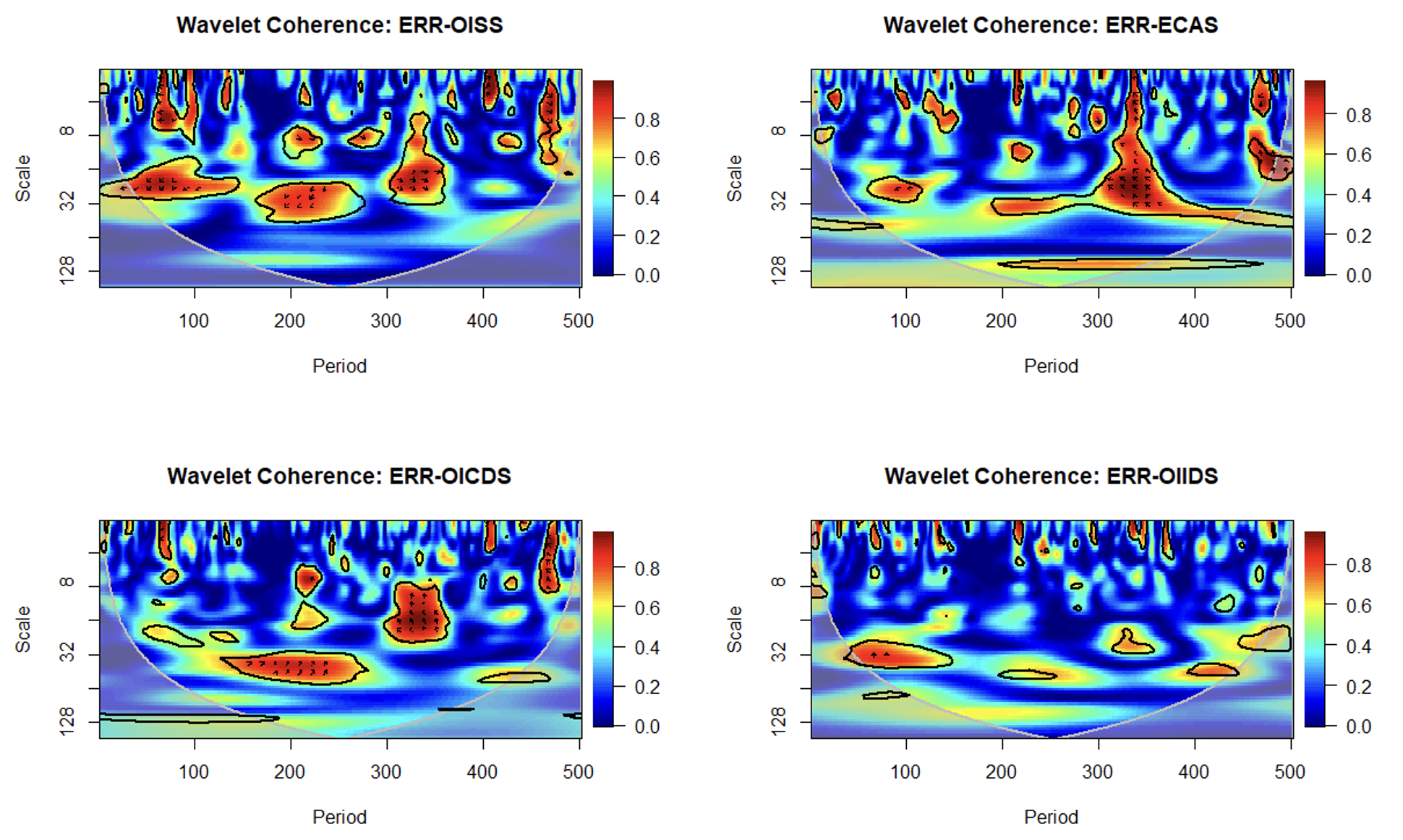

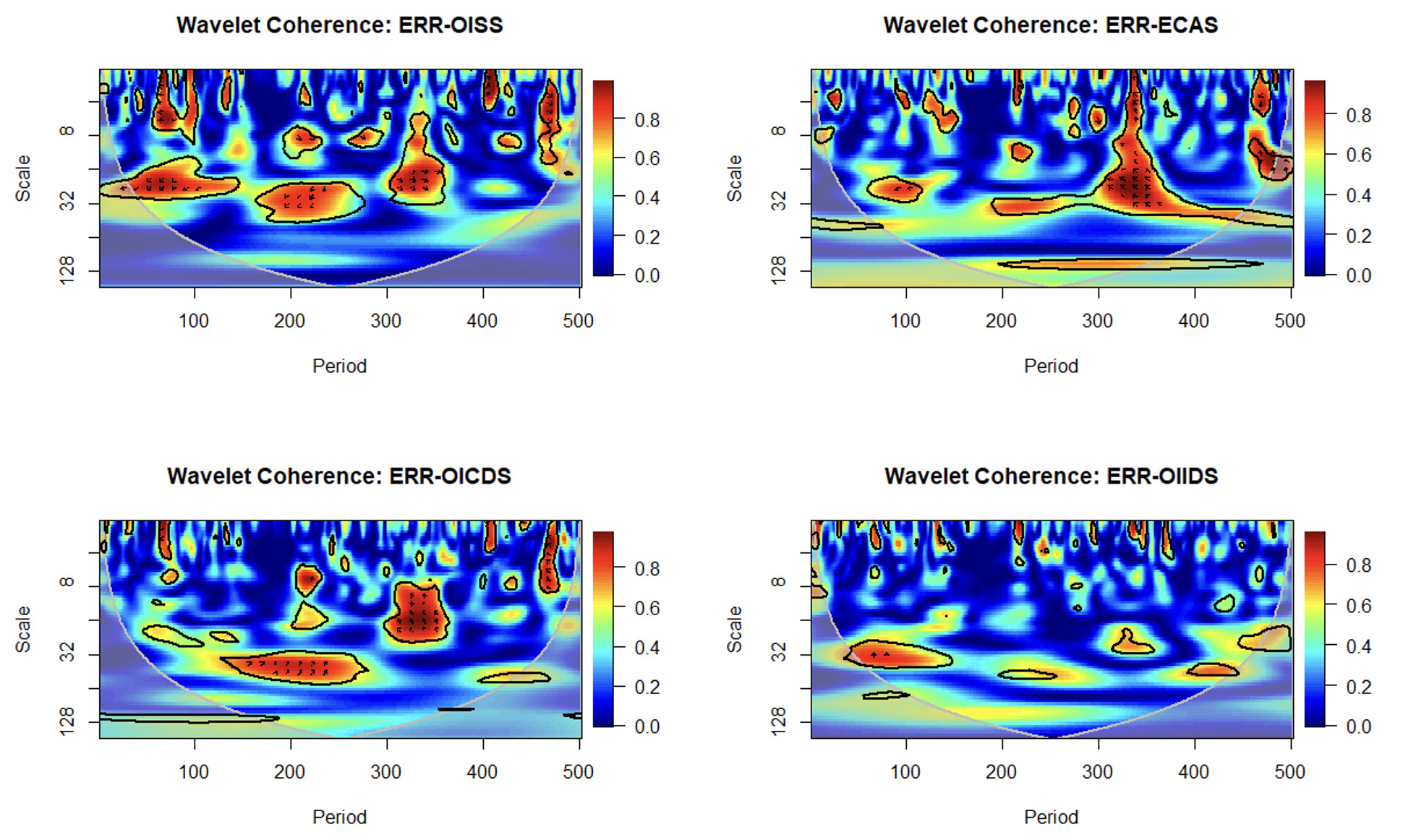

The main findings of the study are reported in Figure 2. The wavelet coherence panel for ERR and OISS reveals a notable interdependent relationship over the period of February 1981 and May 1989 (post-Structural Adjustment Program [SAP] era). We find evidence that OISS is leading while ERR is lagging in the medium-run period, as the arrows point left-down, depicting an anti-cyclical effect. Between the periods of June 1989 and May 2014, there is evidence of bidirectional effects, signaling the interdependent relationship between oil supply shocks and Nigerian exchange rates in the medium-run horizon. Furthermore, it is also evident in the medium-run horizon of June 2014 and December 2022 that while oil supply shocks influenced the Nigerian exchange rates in the early wave of the period, coinciding with the 2014/2015 oil crisis, the leading effect of exchange rates was prominent during the COVID-19 pandemic era. The findings align with the results of Baek (2023) on the heterogeneous effects of oil supply shocks on exchange rates across different countries, indicating country-specific resilience or vulnerability.

In the panel of wavelet coherence for ERR-ECAS, there is a unidirectional effect from economic activity shocks around the period of May 1989 in the medium-run horizon. Simultaneously, there is resounding evidence of a unidirectional effect from the Nigerian exchange rates recorded around February 2006 to May 2014 in the medium-run horizon, corresponding to the global financial crisis period. This reflects evidence of bidirectional effects between Nigerian exchange rates and economic activity shocks within the same frequency horizon. Furthermore, the wavelet coherence plot for ERR-OICDS reveals significant evidence of interdependency mostly in the medium-run horizon, with oil consumption demand shocks signaling a leading effect around the global oil consumption demand shortage of 1985–1986, while a profound leading effect is recorded for the Nigerian exchange rates during the global financial crisis era. This echoes the previous findings from the work of Wang & Xu (2022) and Umar & Rossman (2023) that emphasize the bidirectional causality between oil price shocks and exchange rates. Finally, the fourth panel for the wavelet coherence of ERR-OIIDS reveals no evidence of interdependency between oil inventory demand shocks and the Nigerian exchange rates. This implies an absence of significant causality between both variables over the time-and-frequency domain.

IV. Conclusion

This study explores the interdependency between global oil shocks and Nigerian exchange rates using the wavelet coherence technique. The findings provide multifaceted insights that contribute to a nuanced understanding of the role of global oil shocks in predicting movements in the Nigerian exchange rates. We document evidence of significant interdependency among oil supply shocks, economic activity shocks, and oil consumption demand shocks with the Nigerian exchange rates, primarily during the global financial crisis, the 2014/2015 oil crisis, and the COVID-19 pandemic era, highlighting the country’s vulnerability to global oil market dynamics during pivotal events. However, we find an absence of substantial interdependence between oil inventory demand shocks and the Nigerian exchange rates. Our findings emphasize the significant interdependence between oil shocks and exchange rates, particularly during crucial events, suggesting the importance of economic occurrences in modeling the oil shock-exchange rate nexus in oil-dependent economies.