I. Introduction

The United Nations (UN) has initiated a social development effort aimed at fostering effective partnerships between governments, civil society, and the private sector to achieve social, economic, and environmental targets. These targets include sustaining economic growth, addressing poverty, disease, and natural and man-made disasters, as well as progressing toward stronger international enforcement. Achieving these aims necessitates defining social goals and market institution features that influence market dynamics, especially considering crude oil price risks in a sustainable environment. The increasing demand for energy, particularly crude oil, from developing giants has intensified discussions about global equity capitalization, with the United States (US) maintaining a leading role. This synergy between the crude oil market and the stock market is crucial for creating a stable and functioning institution, despite concerns about the stability of both markets. Understanding the dynamics of these markets under varying crude oil shock intensities can help develop a more stable market.

As the green economy gains prominence, sustainable markets are attracting significant attention from investors, policymakers, and the broader public (Olanipekun et al., 2023). Policymakers are actively offering incentives to promote sustainable investment, while investors are increasingly prioritizing the inclusion of companies that offer environmentally friendly products in their portfolios. In spite of this interest, firms operating in sustainable markets must be profitable enough to attract capital. However, due to the powerful financial characteristics of the crude oil market, risks originating from it can potentially spill over into sustainable markets (Geng et al., 2021). These risks can arise from geopolitical, economic, or financial occurrences. As these risk shocks are transmitted into sustainable markets, they may impact sustainable investments in that sector. Therefore, understanding the interconnectedness between crude oil volatility and sustainable markets is essential, especially for investors to make informed decisions. It is also crucial for governments to develop effective policies that promote sustainable development.

This paper examines the influence of crude oil price volatility on market dynamics within the context of sustainability goals in the US, focusing on the behavior of sustainable stocks. Using a stochastic volatility model, the study assesses how the persistence and conditional distribution parameters of standardized disturbances impacting the crude oil market evolve over time. It analyses the joint evolution of stock and crude oil markets under conditions of heterogeneous new information beliefs, affecting various economic variables over time. The study evaluates sustainable stock market performance within the framework of system sustainability, considering new information shocks affecting both markets.

To empirically assess the impact of crude oil volatility on sustainable market dynamics in the US, the study employs transfer entropy and dynamic connectedness methodologies, using daily data from January 3, 2012, to May 2, 2024. These methodologies capture time-varying relationships and bidirectional information flows, which are crucial for understanding the complex interactions between crude oil and sustainable markets. This comprehensive approach enhances the predictive power of market behavior models and provides a deeper understanding of the interdependencies and dynamic nature of these relationships, contributing methodologically and empirically to existing literature.

II. Data and Methodology

A. Data

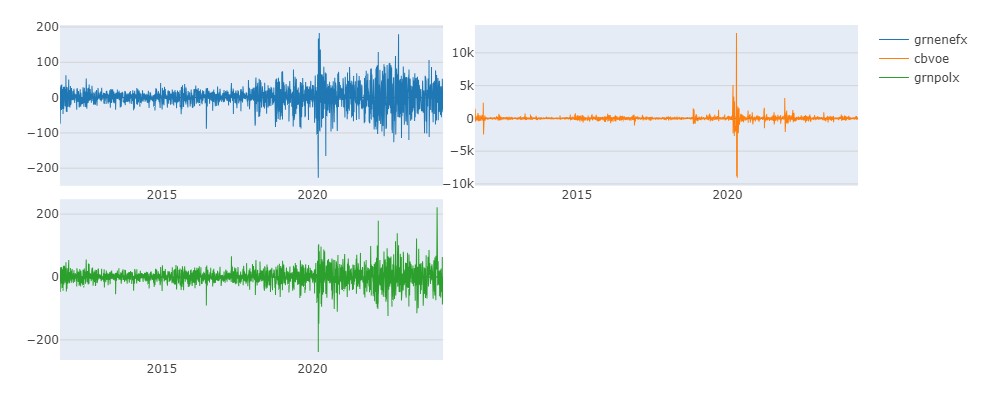

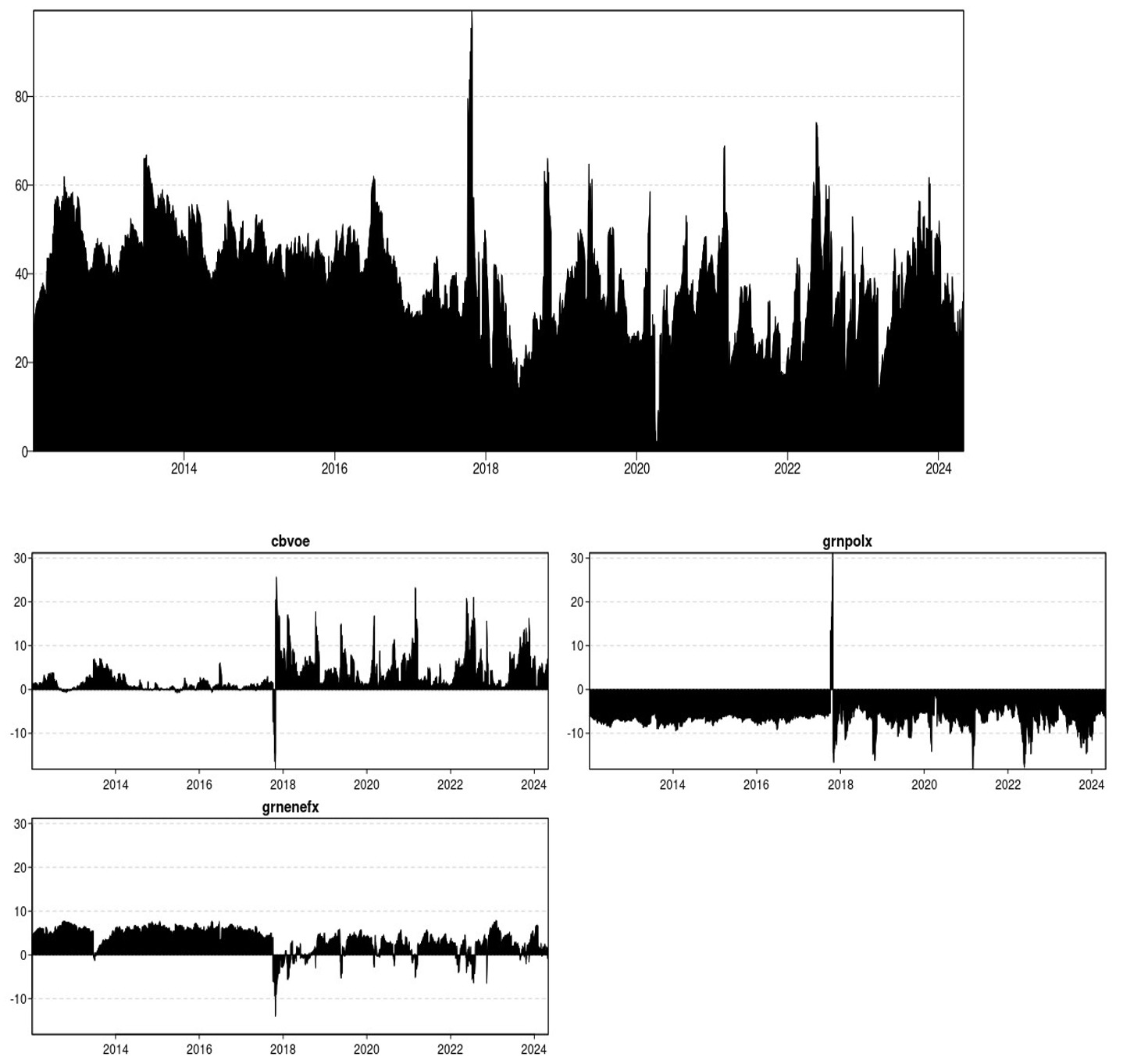

To empirically examine the dynamics of sustainable markets amidst crude oil price volatility in the US, this study analyzes daily data from January 3, 2012, to May 2, 2024, using the Crude Oil Volatility Index (OVX) provided by the Chicago Board of Options Exchange (CBOE) as a measure of crude oil volatility. Unlike traditional GARCH models and historical volatility measures, the OVX, an implied volatility measure, offers a forward-looking perspective by forecasting crude oil price volatility over a 30-day period and capturing investor sentiment. The study measures sustainable markets through the total return indices of the NASDAQ OMX Energy Efficiency (GRNENEFX) and Pollution Mitigation (GRNPOLX) indices, tracking firms that enhance energy efficiency and reduce pollution. The analysis reveals significant volatility, especially during the COVID-19 pandemic, highlighting the impact of major economic disruptions on market dynamics.

B. Methodology

Transfer entropy is a method used to model cause-and-effect relationships in dynamic systems, particularly effective in capturing directional and dynamic interactions within time-series data. Unlike model-based Granger causality and mutual information, transfer entropy handles both linear and nonlinear systems adeptly, capturing types of information that other methods miss. It measures directed asymmetric information transfer between variables non-parametrically. The concept, rooted in Shannon entropy, calculates the entropy of a random variable and combines it with the Kullback-Leibler distance to estimate information flow between processes, assuming a Markov process. This method addresses small sample biases through effective transfer entropy, computed by subtracting the shuffled data transfer entropy. Non-discrete data requires discretization, which is managed via symbolic recording.

To provide additional information on the nature of the relationship between crude oil volatility and sustainable markets, we further employ the Dynamic Conditional Correlation-Generalized Autoregressive Conditional Heteroskedasticity (DCC-GARCH) model of Gabauer (2020). This approach is an improvement on the connectedness approach to modelling risk transmission among variables introduced by Diebold and Yilmaz (2014). Rather than adopting the generalized impulse response function to establish shock impacts, as done by Diebold and Yilmaz (2014), the DCC-GARCH model instead employs volatility impulse response functions to determine shock impacts. The DCC-GARCH approach examines time-varying spillovers via the DCC test, thus circumventing problems associated with the rolling-windows technique employed in the Diebold & Yilmaz (2014) alternative.

III. Results

A. Transfer entropy results

The Shannon transfer entropy and Shannon effective transfer entropy outcomes are reported in Tables 1A and 1B. The estimations are performed with 100 shuffles and 300 bootstrap replications. P-values are calculated by comparing the transfer entropy results to the quantiles of bootstrap samples. The findings indicate that transfer entropy and effective transfer entropy from CBOE to both measures of sustainable markets (GRNENEFX and GRNPOLX) are statistically significant at the 5% level. No statistical significance at any conventional level is recorded in the opposite direction. Transfer entropy assesses the predictive power of variables by measuring how much information about one variable reduces the uncertainty about another variable, beyond what the second variable’s past values can explain. Our results thus demonstrate that information about CBOE decreases the uncertainty about the dynamics of GRNENEFX and GRNPOLX, suggesting that crude oil volatility is valuable for forecasting sustainable development in the US.

Results also suggest that information flow from crude oil volatility to the NASDAQ OMX Energy Efficiency index is almost the same as the flow to the NASDAQ OMX Pollution Mitigation index. Thus, decisions about participation in sustainable markets—whether by households or firms—as well as sustainable development policies by governments, can only succeed when crude oil price volatility is taken into consideration. These findings offer empirical support to studies claiming that oil price volatility and clean energy markets are interlinked (Abdussalam et al., 2022; Asl et al., 2021; Dutta et al., 2021; Lee et al., 2021; Olasehinde-Williams et al., 2023; Yaya et al., 2022) and provide new insights by showing that information about crude oil volatility lowers the degree of uncertainty surrounding sustainable investments.

B. Dynamic connectedness results

We proceed to report and discuss the averaged and dynamic results generated from the DCC-GARCH-based connectedness estimations, which allow us to disaggregate the transmission mechanisms between crude oil volatility and sustainable markets in the US. The results from averaging the dynamic connectedness outcomes, as reported in Table 1C, show a total connectedness index (TCI) of about 32.11% between crude oil volatility and sustainable markets, indicating a significant level of connectedness. Additionally, the results indicate that crude oil volatility transmits the greatest amount of shock to sustainable markets (36.02%) and receives the least amount of shock from them (18.91%). Negative net directional connectedness values for sustainable markets imply that they are net receivers of shocks from crude oil volatility, while the positive value for crude oil volatility indicates it is a net transmitter. Furthermore, GRNENEFX receives more shocks from crude oil volatility (41.26%) than GRNPOLX (36.16%). These findings contradict those of Henriques & Sadorsky (2008) and Ahmad (2017), who found no evidence of oil market volatility transmission to clean energy firms and classified crude oil as a net receiver, respectively. However, they support studies such as Asl et al. (2021), Dutta et al. (2021), Abdulsalam et al. (2022), Yaya et al. (2022), and Olasehinde-Williams et al. (2023).

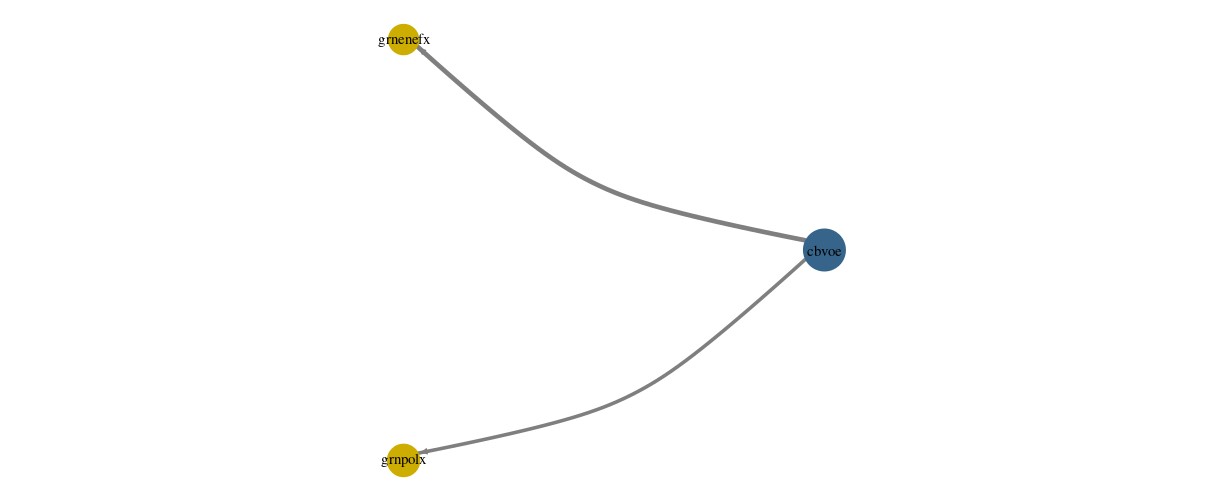

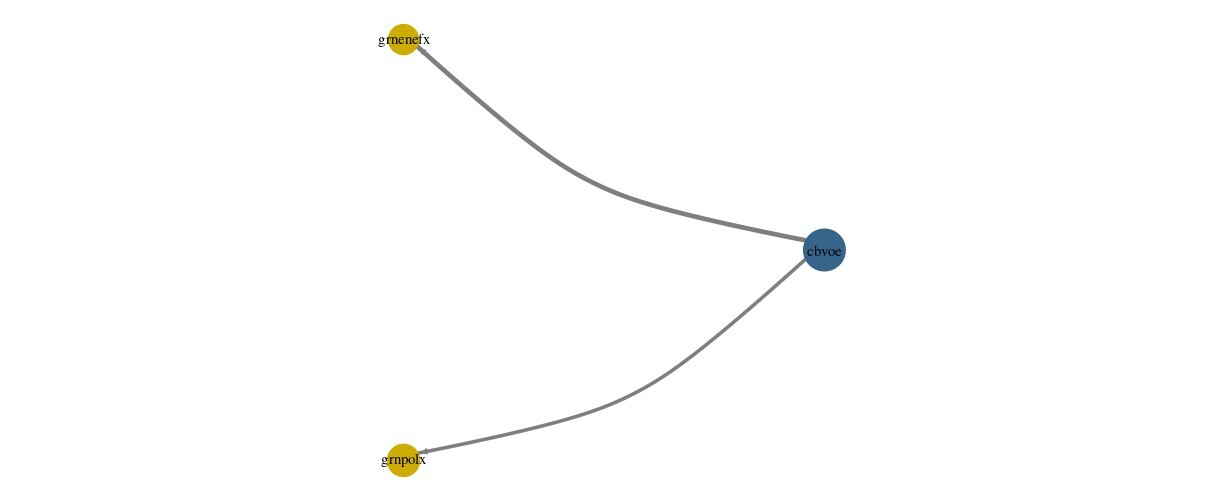

The averaged results in Table 1C do not account for time-specific variations, so we further analyze the DCC-GARCH-based dynamic connectedness plot in Figure 2, which shows dynamic TCI ranging mostly between 20% and 65%. This indicates that the dynamic TCI among crude oil volatility and sustainable markets is relatively strong and time-varying, with significant risk spillovers during events such as the Saudi-US oil conflict, the Russo-Ukraine conflict (2014-2016), financial crises (2017-2019), the 2018 stock market crisis, and the COVID-19 pandemic. Figure 2 shows that CBOE is the major net risk transmitter, while GRNPOLX and GRNENEFX are net risk receivers, confirming crude oil volatility as a primary source of risk spillover into sustainable markets. The network plot of net pairwise directional connectedness in Figure 3 illustrates that CBOE (blue) is the net transmitter and GRNENEFX and GRNPOLX (yellow) are net receivers. The thicker line connecting CBOE to GRNENEFX indicates a more intense connection, revealing that crude oil volatility transmits shocks to sustainable markets, with the NASDAQ OMX Energy Efficiency index being more susceptible to these shocks than the NASDAQ OMX Pollution Mitigation index.

IV. Conclusion and Policy Recommendations

The impact of contagion spillovers between financial markets has become a significant concern as the world economy becomes increasingly integrated. As such, policymakers and investors need to make critical decisions and develop action plans on how to engage with the relatively new sustainable financial markets. Therefore, understanding the transmission mechanisms in these growing markets is crucial. To this end, this study evaluates sustainable market dynamics under crude oil volatility in the US by examining the dynamic connectedness between crude oil volatility and sustainable markets in the country. Transfer entropy results suggest that crude oil volatility is valuable for forecasting sustainable market dynamics, and DCC-GARCH analysis reveals dynamic risk spillovers, especially during key geopolitical and economic events.

The findings have important implications for stakeholders. First, since crude oil acts as a source of risk for sustainable markets, policy measures should be implemented to mitigate the impact of increased volatility in the oil market. Second, insights from crude oil markets are valuable for making informed decisions about sustainable investments. Risk managers and portfolio managers must account for the significant spillover effects from crude oil into sustainable investments when predicting portfolio returns. Third, the level of risk connectivity between crude oil and sustainable investments fluctuates over time and intensifies during crises. These uncertainties should be carefully integrated into portfolio strategies by risk managers and portfolio managers. Lastly, given the continued reliance of the US on crude oil, high volatility transferring from oil markets to sustainable investments is likely to be a recurring issue. Therefore, the government should ensure adequate support for companies involved in sustainable products.