I. Introduction

Recently, energy and other precious metals commodities have gained significant financial importance, particularly during times of financial crises. While gold, silver, and other precious commodities are widely recognized as financial assets, metals such as cobalt, copper, lithium, and nickel are increasingly vital for advancing the global energy transition (see Balcilar, Usman, & Agan, 2024). According to the real options theory and supported by existing empirical literature, greater economic policy uncertainty (EPU) appears to impact not only market conditions, firm investment, and financial policies, but also the decisions taken by investors and households. For example, when EPU increases, the firms’ willingness to invest and hire workers as well as the households’ willingness to consume goods and services, tend to decline, as they prefer to postpone investments and consumption (Balcilar, Usman, & Duman, 2024; Bloom, 2014; Usman et al., 2024).

Although studies have investigated the drivers of demand-supply dynamics of critical mineral commodities (Jowitt & McNulty, 2021; Renner & Wellmer, 2020) and the causal nexus between the energy transition metals and other minerals, especially non-metallic minerals (Yahya et al., 2020; Zhang et al., 2023), the role of economic policy uncertainty (EPU) associated with cable news, i.e., Cable News-based EPU (TVEPU) on both energy and precious metals commodities has not been explored in the literature. As noted by the Pew Research Center, about 16 percent of American residents cite cable news networks as their main source of political information while print media (i.e. newspaper-based EPU) constitutes only 3 percent (see Bergbrant & Bradley, 2023). If investment decisions of firms and individual investors in energy and precious metals commodities are influenced by cable news-based networks rather than newspapers, then applying newspaper-based EPU would generate incorrect outcomes, as demonstrated by Adebayo et al. (2024). Therefore, this study contributes to the existing literature in two significant ways: First, the study investigates the predictive content of the EPU extracted from cable news, otherwise known as TVEPU for energy and precious metals commodities. Second, the study applies a novel Wavelet Nonparametric Quantile Causality (WNQC) test, which captures the causal effect across time and quantiles simultaneously. Therefore, the outcome of this investigation would not only inform policymakers and investors on the issues of energy and metallic commodities markets, but it can also further guide stakeholders in the media space on news reportage.

The structure of this study is outlined as follows: Section II details the data description and empirical methods; Section III discusses the empirical results; and Section IV presents concluding remarks along with policy recommendations.

II. Data and Methodology

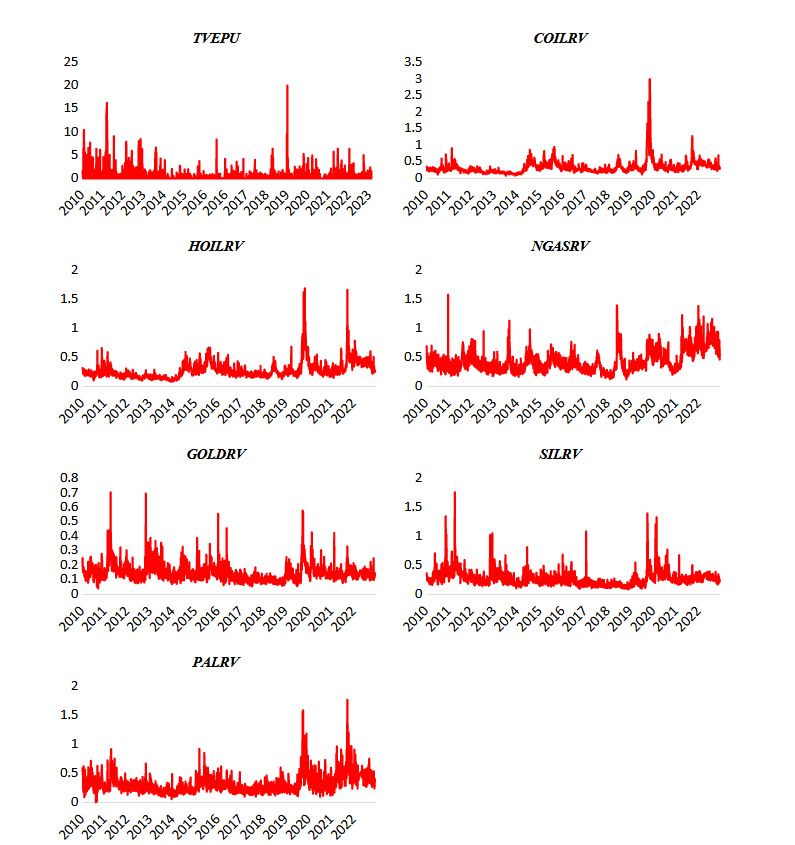

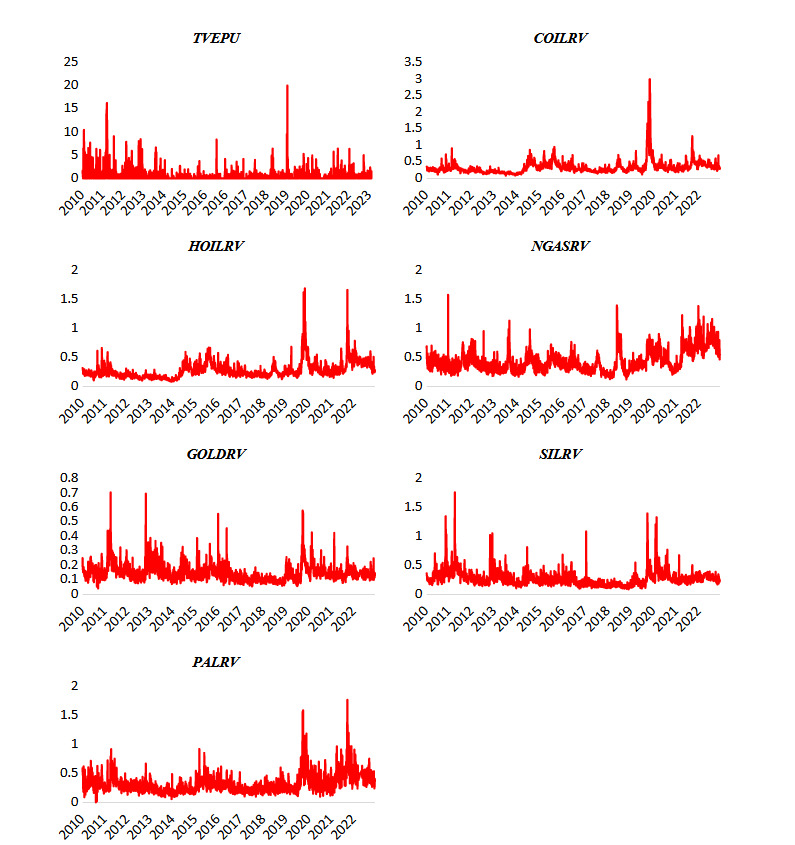

We investigate the time-quantile causal effects of Cable News-based EPU (TVEPU) on the realized volatility (RV) of energy and precious metals commodities using the longest available daily data series from 01/07/2010 to 26/05/2023. The TVEPU series was computed by Hong et al. (2021) and Bergbrant & Bradley (2023) from the major US cable news networks (i.e., CNN, Fox News, and MSNBC) using AI with selected keywords. We obtain the TVEPU data from https://www.policyuncertainty.com. Furthermore, we use crude oil (COIL), heating oil (HOIL), and natural gas (NG) as energy commodities, and gold, silver (SIL), and palladium (PAL) as precious metals commodities. The RV data for the energy and precious metals commodities are downloaded from https://dachxiu.chicagobooth.edu/#risklab. Figure 1 shows TVEPU and RV series, and Table 1 provides their summary statistics.

Table 1, Panel A, shows that TVEPU has a higher average and is more volatile than the RV series. Among the RV series, NGASRV has the highest average, while COILRV exhibits the most volatile behavior. In contrast GOLDRV has the lowest average and is the least volatile. TVEPU and all RV series are positively skewed and leptokurtic, i.e., non-normally distributed, as confirmed by the Jarque-Bera test. Finally, the TVEPU and RV series are stationary. Moreover, the non-linear nature of these series is also empirically confirmed by the nonlinearity (BDS) test (see Table 1, Panel B). The non-normal and non-linear characteristics of TVEPU and RV series suggest that the use of linear methods in this study may produce misleading results.

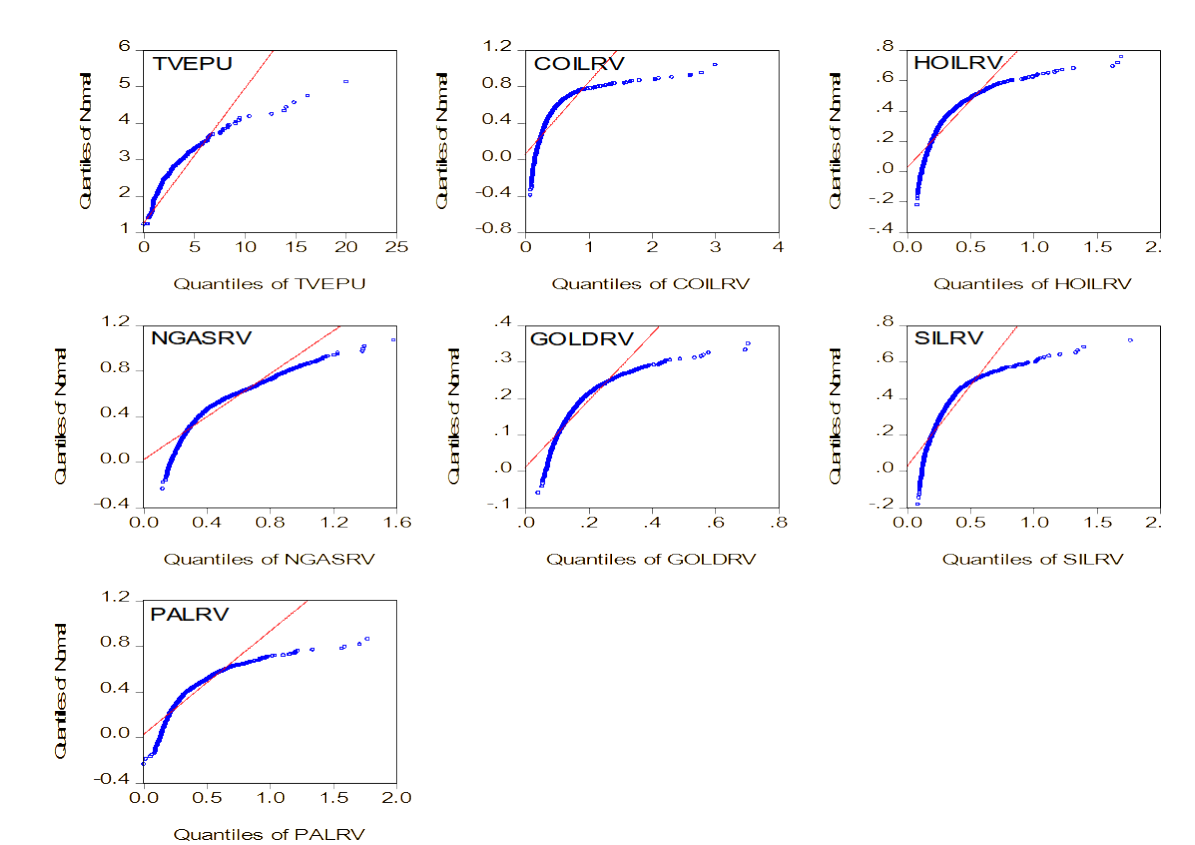

It is evident from the normality (QQ) plots shown in Figure 2 that TVEPU and all RV series exhibit non-linear features.

_plots.png)

Considering data series features, this study employs the innovative non-linear causality method of Wavelet Nonparametric Quantile Causality (WNQC) by Adebayo & Özkan (2024) in the empirical analysis. The WNQC analyzes the causal dependency structure between two stationary series in their means and variances across different quantiles and time periods within the framework of a nonparametric procedure, which minimizes the misspecification error. Therefore, unlike the nonparametric quantile causality developed by Balcilar et al. (2016), the WNQC allows us to determine not only how the causality in means and variances of TVEPU and energy and precious metals commodities RV changes across quantiles but also across timeframes. In this case, the WNQC test addresses the potential variation in causal relationships both in mean and variance across different time scales. The hypotheses of WNQC in mean and variance from TVEPU to RV of energy and precious metals commodities at the -th quantile and -th period can be specified as follows:

H0:P{Fdp[RV1,2i,t]∣dp[Xt−1]{∅(q)(dp[RVi,t−1])∣dp[Xt−1]}=q}=1

H1:P{Fdp[Rv1,2i,t]∣dp[Xt−1]{∅(q)(dp[RVi,t−1])∣dp[Xt−1]}=q}<1

where is the -th period series of the -th commodity, represents the quantiles, and is the vector of TVEPU and RV series. The WNQC calculates the feasible test statistic to test the hypotheses in Equations (1) and (2) as follows:

ˆJμ=1μ(μ−1)w2γμ∑t=γ+1μ∑c=γ+1,c≠tK

where denotes bandwith, represents the lag length, and indicates the sample size.

III. Empirical Results and Discussion

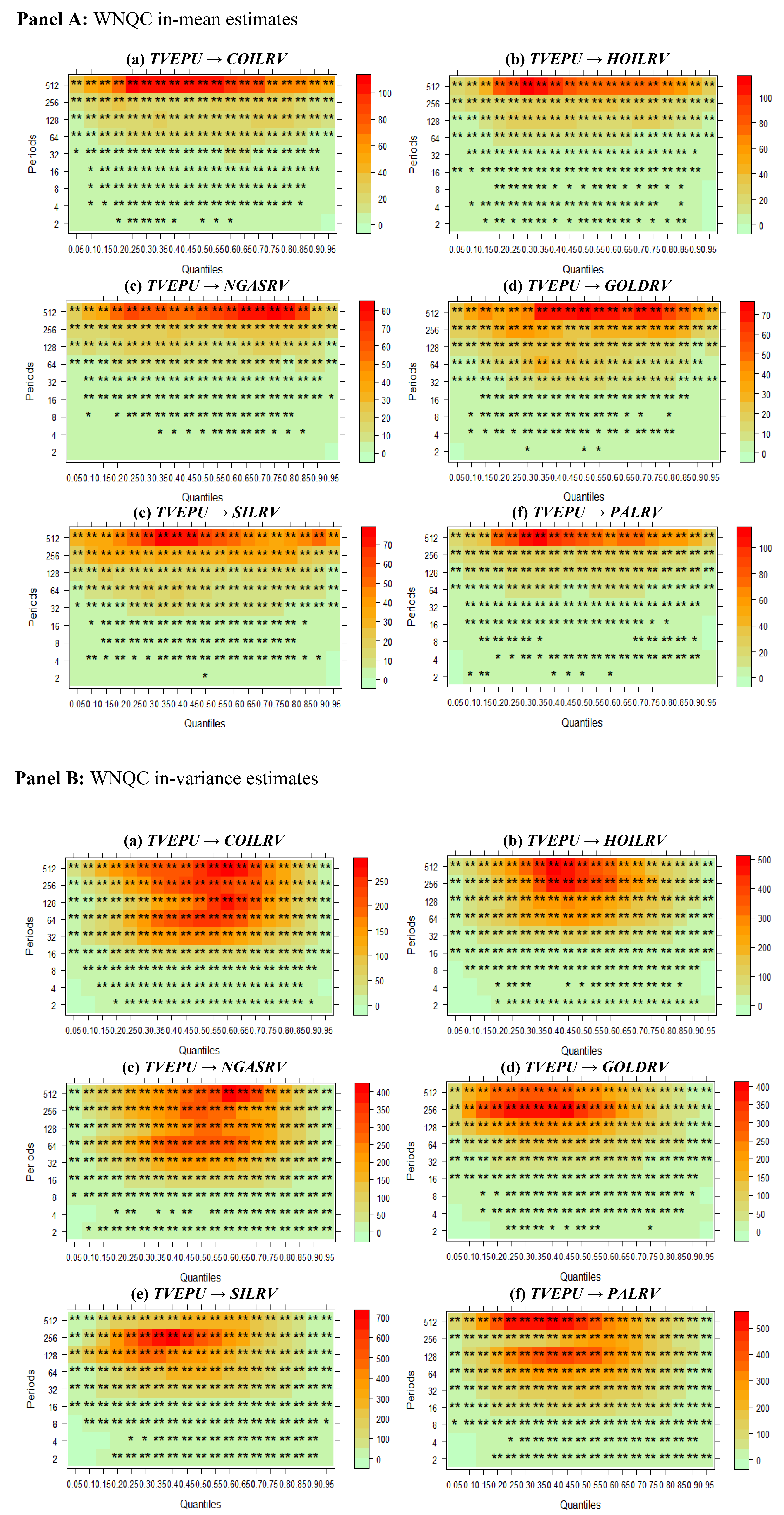

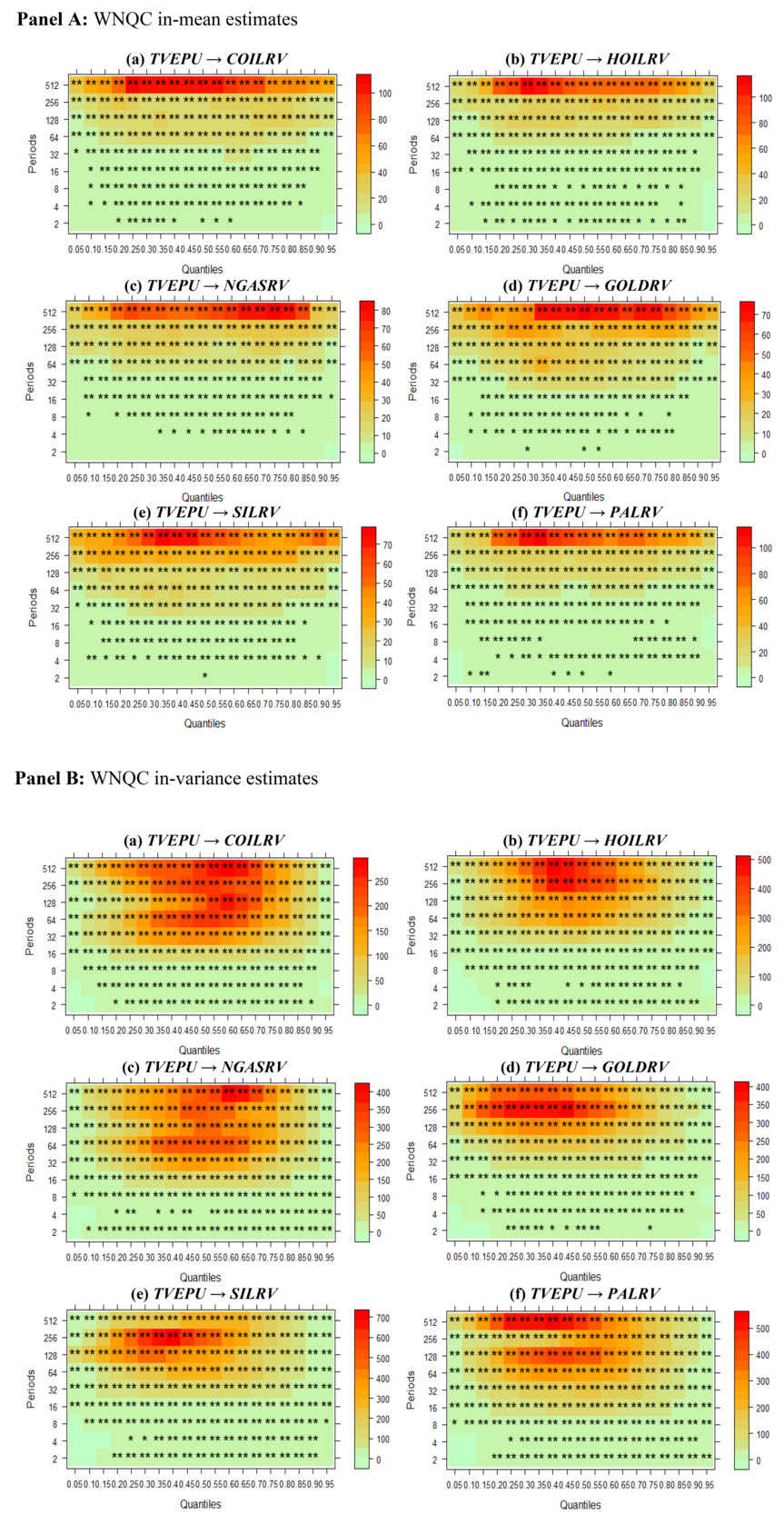

To investigate the time and quantile causality between TVEPU and energy commodities and precious metals, we apply the newly developed WNQC method. The results reported in Figure 3 demonstrates the predictive ability of TVEPU for both energy commodities and precious metals in-mean and in-variance, respectively. Specifically, Figure 3 (Panel A), presents results of the WNQC in-mean. The figure shows evidence of TVEPU’s predictive ability for both energy commodities and precious metals across different periods and quantiles. The results indicate that the strength of TVEPU’s predictive power decreases from higher periods to lower periods. Furthermore, TVEPU has no predictive content for energy commodities and precious metals in the tail quantiles between the periods of 2 to 32, with this effect being more pronounced in the lower periods.

For variance, the results are presented in Figure 3 (Panel B). The results provide evidence of a time and quantile causal effect of TVEPU on energy commodities and precious metals. In other words, TVEPU’s predictive power is evident for both energy commodities and precious metals. Similar to the WNQC in mean, the predictability of TVEPU for all categories of energy commodities and precious metals is stronger in higher periods and declines across the middle and lower periods. For energy commodities and precious metals, we find no evidence of causality in the tail quantiles for the lower periods (2 to 8), although causality is observed in the middle and higher periods for all quantiles. Additionally, we find that the predictive power of TVEPU for energy commodities and precious metals in causality-in-variance is stronger than in causality-in-mean.

These results imply that the predictive content of TVEPU exhibits a significant heterogeneity, resulting in non-linearity across periods and distributions of energy commodities and precious metals. Our findings therefore suggest that shocks in TVEPU affect energy commodities (such as crude oil, heating oil, and natural gas) and precious metals (such as gold, silver, and palladium). For instance, a lower level of TVEPU appears to stimulate firms’ willingness to invest in energy commodities and precious metals, and consumers’ spending on these commodities. Thus, our results align with Balcilar et al. (2021), who show that EPU measures are predictors of bond spreads in both lower and higher quantiles, with predictability in causality-in-variance being stronger and greater than causality-in-mean. The weaker predictive power of EPU in lower quantiles and periods is consistent with Balcilar et al. (2016), who applied nonparametric causality in quantiles to test the predictability of uncertainty for gold returns and volatility. However, our findings extend beyond existing studies by incorporating standard Nonparametric Quantiles Causality-in-mean and variance (NQC) to capture wavelet pairs, accounting for both time scale and quantiles simultaneously. Thus, the unequal predictive power of TVEPU for energy and precious metals commodities across quantile distribution is based on time and quantiles, differentiating it from the existing literature, such as Balcilar et al. (2016), Yahya et al. (2020), and Zhang et al. (2023), which relies on nonparametric causality in quantiles and cross-quantile analysis.

IV. Conclusion

This study examines the predictive power of TVEPU for the realized volatility of energy commodities (crude oil, heating oil, and natural gas) and precious metals (gold, silver, and palladium) using the innovative Wavelet Nonparametric Quantile Causality methodology, covering the period from 01 July 2010 to 26 May 2023. We confirm TVEPU’s predictive power for both energy and precious metals commodities, in terms of mean and variance. The predictability of TVEPU is stronger in higher periods and diminishes in lower periods, particularly at the tail quantiles. This suggests that TVEPU’s predictive power for these commodities follows a non-linear pattern. Understanding how energy and precious metals commodities respond to TVEPU across different times and quantiles can help market participants optimize portfolio diversification and strengthen their hedging strategies. For instance, lower levels of TVEPU appear to increase firms’ willingness to invest in these commodities and households’ spending on them. Our findings could also improve the stability of energy and precious metals markets by reinforcing resilience, especially in the face of uncertainties arising from cable news networks, through informed policy decisions.