I. Introduction

With the acceleration of globalization and the dynamic changes in the energy market, fluctuations in oil prices not only directly affect the welfare of energy-intensive industries and consumers but also impact international trade, monetary policy, and investment decisions through various channels (Ilyas et al., 2021). However, fluctuations in oil prices remain one of the major challenges faced by the global economy. These fluctuations are influenced not only by traditional supply and demand dynamics but also by frequent geopolitical events, policy changes in oil-producing countries, and global market sentiments (Jiao et al., 2023). In recent years, economic policy uncertainty (EPU) has emerged as a new and increasingly impactful factor affecting the oil market. EPU refers to uncertainty regarding future government policy actions and their effects on the behaviour of economic agents (Zhang et al., 2023). This uncertainty can arise from various aspects, such as fiscal policy, monetary policy, and trade policy, having profound effects on corporate investment decisions, consumer spending, and overall economic activity. In this context, an increase in EPU often leads to heightened risk aversion among market participants, affecting global capital flows and investment trends and thereby causing fluctuations in oil prices (Fang et al., 2023).

Existing literature has extensively studied the impacts of EPU on overall fluctuations in oil prices (Lin & Bai, 2021; Liu et al., 2023). Lin and Bai (2021) employ a time-varying parameter vector autoregression model to examine the impacts of EPU in oil-importing and oil-exporting countries on fluctuations in oil prices, finding that the negative impacts of EPU in oil-exporting countries on oil price volatility are greater than that in oil-importing countries. Liu et al. (2023) use an exponential generalized autoregressive conditional heteroskedasticity mixed data sampling approach to investigate the effects of EPU on oil price volatility and discover that EPU has a negative effect on oil price volatility. However, current research overlooks the dynamic changes in the oil market that can be driven by various factors, such as variations in the supply and demand of oil. Seemingly similar oil price increases or decreases may be supported by different forces. Therefore, studying overall oil price volatility alone may obscure heterogeneous responses and the accumulation of related risks (Feng et al., 2023). Thus, this study aims to investigate how EPU affects oil shocks from various sources, addressing the gaps in the existing literature.

The contributions of this paper are as follows. Firstly, this paper is the first to employ a cross-quantilogram approach to study the effects of EPU on oil shocks from different sources. The decomposition approach proposed by Ready (2018), used in this paper, can accurately decompose oil shocks in terms of the three dimensions of supply, demand, and risk. The cross-quantilogram approach enables the assessment of directional predictability and serial dependence between different scales of two data series by setting different lag orders. Secondly, this paper’s research on the spillover effects of EPU on oil shocks from different sources not only aids policymakers in formulating more effective macroeconomic policies and energy strategies but also provides references for financial investors making informed investment decisions in complex market environments.

The rest of this study is structured as follows. Section II describes the econometric methods used, while Section III introduces the data and conducts a basic data analysis. Section IV provides empirical findings of this study. Finally, Section V provides concluding remarks.

II. Methodology

A. Oil price decomposition method

Following the method proposed by Ready (2018), we decompose oil shocks into supply shock (SS), demand shock (DS), and risk shock (RS). Based on the assumption of orthogonality among the three different sources of shocks, the equation can be

Xt≡[ΔoiltRProdtξVIX,t], Zt≡[sstdstrst], A≡[1110a22a2300a33]

where denotes the return in oil price, represents the return of the global stock index for oil-producing companies, and signifies the VIX innovation values based on specification. is a 1 × 3 vector, where represents supply shock, denotes demand shock, and signifies risk shock. The matrix maps the shock vector to :

Xt=AZt

B. Cross-quantilogram approach

The cross-quantilogram approach can assess the directional predictability and serial dependence across various quantiles of two data series without necessitating any conditional moments of the time series. This makes it particularly well-suited for financial time series analysis (Han et al., 2016). The method is defined as follows:

Pα=E[φα1(x1, t−q1(α1))φα2(x2,t−k−q2(α2))]√E[φ2α1(x1,t−q1(α1))]√E[φ2α2(x2,t−q2(α2))]

where represents a quantile-based cross-correlation estimator, which is employed to illustrate the response of oil shocks to EPU. signifies the time lags. denotes the quantile-striking process. serves as an indicator parameter.

III. Data

This paper decomposes the raw data of three different sources of oil shocks, which are NYMEX crude-light sweet oil futures, S&P Commodity Producers Oil and Gas Exploration and Production Index, and CBOE volatility index. These correspond to supply, demand, and risk shocks, respectively. The three sets of raw data originate from DataStream, S&P Global, and the Chicago Board Options Exchange. Additionally, this paper employs the World EPU index, which can be accessed on the Economic Policy Uncertainty website. The data in this paper consists of daily data, covering the period from December 19, 2005, to January 5, 2024. Descriptive statistics for each variable can be found in Table 1. Every check for normality, like skewness, kurtosis, and the J-B test, indicates that the variables involved in this paper are non-normally distributed. Furthermore, the results of the ERS test confirm that the series of each variable is stationary.

IV. Empirical Results

A. Cross-quantilogram results

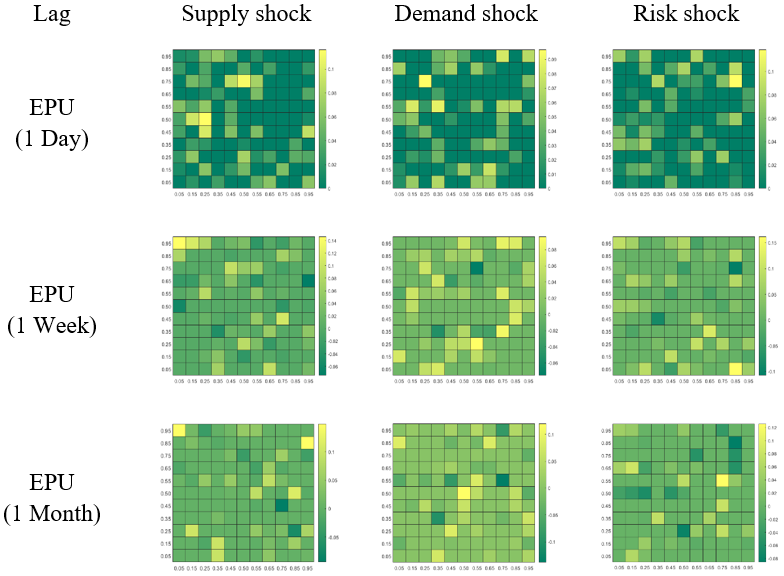

This section presents the results of the cross-quantilogram method. Notably, this study also considers lags of daily (1 day), weekly (5 days), and monthly (22 days) durations to assess the short-, medium-, and long-term risk spillover effects. Figure 1 displays the response of three different sources of oil shocks to EPU over various lag periods. Initially, EPU positively affects all three different sources of oil shocks in the short term. This finding is consistent with that of Li et al. (2023), suggesting that the dominance of short-term speculation during periods of unclear economic policy direction positively impacts EPU.

Moreover, over time, the positive effect of EPU on oil shocks from different sources gradually diminishes and eventually turns negative in the medium and long term. This observation is akin to the findings of Adedoyin and Zakari (2020), indicating that EPU hinders medium and long-term economic planning and structural adjustments, thereby adversely affecting economic growth and development. Lastly, the study finds that the negative effect of EPU on risk shocks is most pronounced in the medium and long term. This is attributed to risk shocks being derived from the VIX index, which reflects market participants’ expectations of future market volatility. The adverse effect of EPU in the medium and long term negatively influences market participants’ expectations, leading to a more severe negative impact on oil risk shocks.

B. Robustness check

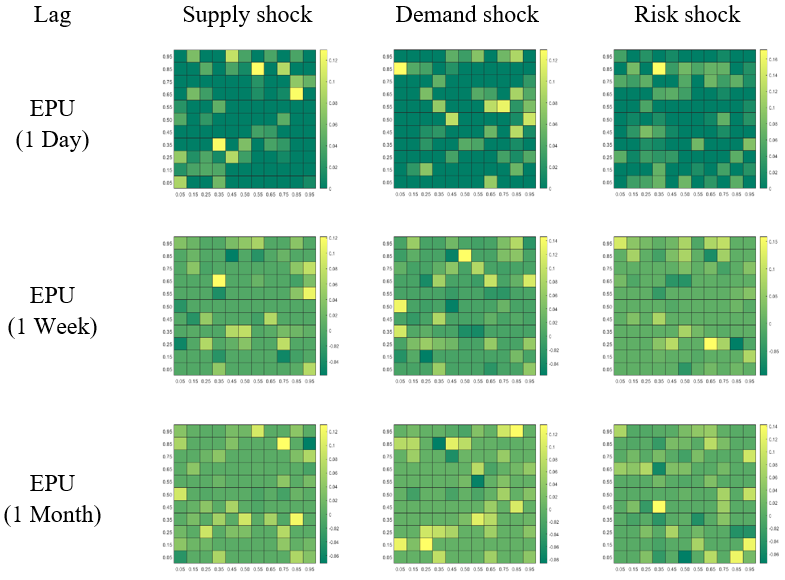

This study considers substituting the main variables in empirical research to recalculate the results of the cross-quantilogram method as a robustness test. Specifically, this paper uses Brent crude oil futures instead of NYMEX crude-light sweet oil futures. This is because Brent crude is one of the main benchmarks in the international oil market and is widely used in the pricing of global oil trading. Moreover, this paper also adopts the CBOE NASDAQ-100 Volatility Index (VNX) in place of the CBOE Volatility Index (VIX). This choice is made because the VIX reflects the implied volatility based on options of the Standard & Poor’s 500 Index, which mainly covers multiple sectors including finance, consumer goods, and energy. In contrast, the VNX stems from the implied volatility of options of the NASDAQ 100 Index, focusing more on large-cap stocks in technology and non-financial sectors. Therefore, using VNX as an alternative variable for robustness testing can enhance the broader applicability and reliability of this study. The sample interval controlled in this section is from December 19, 2005, to January 5, 2024, consistent with the main analysis. Figure 2 shows the recalculated results of the cross-quantilogram method. As can be seen from Figure 2, the recalculated risk spillover results are generally consistent with the previous analysis, verifying the robustness of our results.

V. Conclusion

This article investigates the short-, medium-, and long-term risk spillover impacts of EPU on oil shocks from three different sources using the cross-quantilogram method. Initially, EPU has a positive effect on oil shocks from all three sources in the short term. In addition, the positive impact of EPU on the three different sources of oil shocks diminishes and eventually turns negative in the medium and long term, with the most severe negative impact observed for the oil risk shock. The paper’s empirical results could be significant for policymakers and financial investors. For policymakers, it is advisable to maintain flexibility in designing and implementing economic policies to leverage this short-term effect in supporting the stability of the oil market. Furthermore, policymakers should aim to reduce EPU by establishing a clear long-term policy framework and a stable policy environment, thereby supporting the long-term stability of the oil market and investor confidence. For financial investors, it is important to consider the short-term positive impacts of EPU and adjust their short-term investment strategies accordingly to capitalize on market fluctuations for potential gains. Conversely, adopting a long-term perspective, considering diversified investment portfolios, and employing hedging strategies can help mitigate potential market risks.